Opportunities and pitfalls: The Ruffer guide to family investments in 2020

How should global business families of wealth navigate the choppy investment waters in the year ahead? Is a global economic recession looming and what does that mean for family investors? Emma Rutter, investment director at Ruffer LLP, urges diversification in portfolios, says environmental, social and governance (ESG) criteria should be a prism to view all investments through and explains why “liquidity will be king”.

Where does Ruffer see investment opportunities in 2020?

UK assets look exciting post-general election. Whatever one thinks of the politics, Boris Johnson’s Conservatives have broken the political deadlock and have an ambitious pro-market economic reform agenda. British businesses and assets stand poised to benefit from increasing political clarity, simultaneous monetary and fiscal stimulus, and improving sentiment among global investors. And starting valuations are modest relative to the rest of the world.

Japanese equities are also exciting. Despite strong growth prospects and asset-rich balance sheets, their stock often trades at what we think are excessively discounted valuations to their global peers.

UK and Japanese stocks are now the largest element of our equity position.

What are the investment pitfalls to watch out for?

What are the investment pitfalls to watch out for?

After a decade of unprecedented distortions wrought by extreme monetary stimulus—quite a few!

Corporate credit looks dangerous: quantity has ballooned whilst quality has declined markedly. Much of it is held in vehicles which promise share-like liquidity (ETFs), but the underlying assets are fundamentally illiquid. With the enormous expansion in passive trackers, this mismatch is a real threat to the market.

So liquidity, or rather illiquidity, is the central risk: investors should be vigilant about what Jonathan Ruffer terms ‘mouse-trap’ investments—ones that are easier to get in to rather than out of.

Inflation is a long-forgotten foe. Yet it seems to us that structural deflationary forces are weakening whilst unemployment is at record lows and wages are growing. As monetary and fiscal policy become ever more expansionary and the global economy turns, an inflation shock is a real risk. Ruffer portfolios hold protective assets that look to guard against all such menaces.

Inflation is a long-forgotten foe. Yet it seems to us that structural deflationary forces are weakening whilst unemployment is at record lows and wages are growing. As monetary and fiscal policy become ever more expansionary and the global economy turns, an inflation shock is a real risk. Ruffer portfolios hold protective assets that look to guard against all such menaces.

Is a global economic recession likely to hit markets in 2020?

It’s possible but, as things stand, unlikely. The US Federal Reserve’s volte-face at the end of 2018 has been followed by easier monetary policy globally, and this will continue throughout 2020. Many governments are considering large-scale fiscal stimulus, which could provide a further tailwind. Our bias therefore is that any ‘surprise’ will likely be a positive one, so hard-pressed areas of industrial economies could see fortunes improve. As a result, we hold economically-sensitive cyclical stocks, which stand poised to benefit from any improvement in, or continuation of, global growth.

What can families of wealth do to mitigate their exposure to a recession?

What can families of wealth do to mitigate their exposure to a recession?

Start by holding enough cash to cover short and medium-term spending commitments, reducing the risk of being a forced seller of assets at precisely the wrong moment. Liquidity will be king. We complement traditional defences with truly diversifying assets—derivative instruments that will gain if market volatility increases, equity markets experience severe or sharp falls, or yields rise on corporate debt.

Should family investors diversify or concentrate their investments?

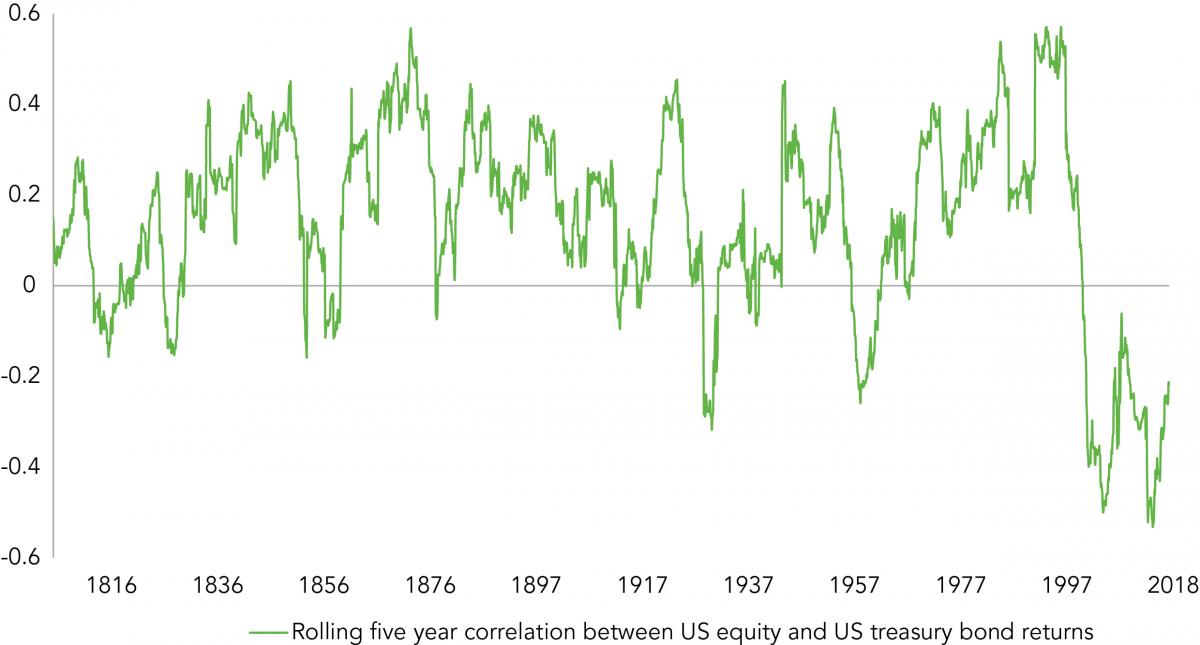

We would encourage family investors to ensure that they are truly diversified—and this is particularly true when a large portion of their wealth is invested in an operating business which brings natural concentration. We fear that, having risen together, all assets could fall together. The negative correlation between stocks and bonds which has served balanced portfolios so well in recent decades, could return to historic normality, as shown in the graph below. Ruffer approaches diversification not through backwards-looking statistical measures, but rather a broad assessment of how different assets may behave in foreseeable scenarios. Doing so has helped us preserve and grow capital since inception in 1994, including during the Credit Crunch.

Source for chart: Source: Datastream; Global Financial Data (GFD); Ruffer calcs

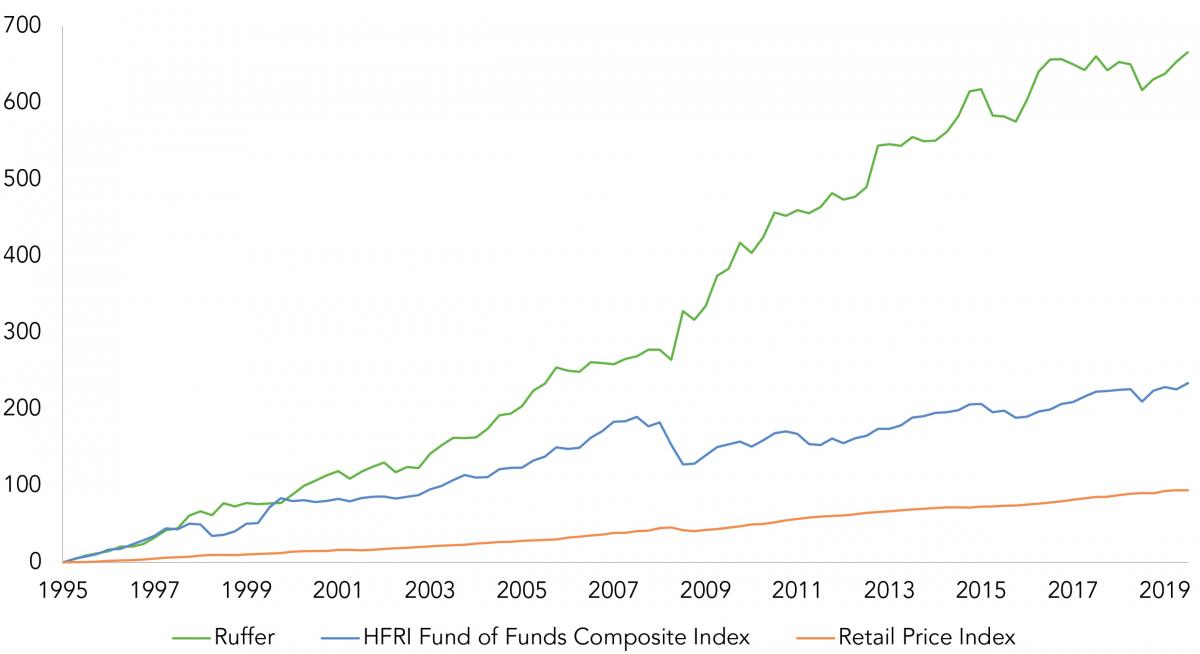

Is this a good time for families to increase their allocation to alternative investments?

Yes. But what those alternatives are really matters. Many alternative asset classes (e.g. private equity) have also seen huge price increases, and often invest in illiquid underlying assets. We think illiquidity could be at the epicentre of the next crisis and that many so-called alternatives will prove to be both riskier and more highly correlated with listed markets than expected. At Ruffer, we have an alternative approach that has driven returns uncorrelated with wider markets while holding a portfolio of liquid assets at considerably less cost than typically paid in, for example, hedge funds or private equity.

Source: Ruffer, HFRI, Thomson Datastream

Should families maximise their ESG investments at a time of economic uncertainty?

ESG should not be a sub-category of an investment strategy. ESG is a prism through which to view all investments—and one which can boost returns. As long-term custodians of clients’ assets, Ruffer regards ESG as an essential discipline which is integrated throughout our investment process—and has been for years.

How can families make the most impact through ESG and responsible investing in 2020?

How can families make the most impact through ESG and responsible investing in 2020?

Engage, don’t divest! Walking away just leaves returns on the table for less scrupulous investors.

Ruffer LLP will attend the Campden Wealth Family Alternative Investment Meeting in London on 25-26 February and the Family Office and Investment Conference in Geneva on 12-13 May.

Ruffer is a limited liability partnership, registered in England with registered number OC305288 authorised and regulated by the Financial Conduct Authority © Ruffer LLP 2020. The views expressed in this article are not intended as an offer or solicitation for the purchase or sale of any investment or financial instrument. The information contained in the document is fact based and does not constitute investment advice or a personal recommendation, and should not be used as the basis for any investment decision. References to specific securities should not be construed as a recommendation to buy or sell these securities.