Fixed income needn't be so taxing

The most challenging investment tax issues can often be found in an investor’s fixed income allocation, say the experts in family office, global tax and investments at Wellington Management. They explore some of the strategies available to investors.

KEY POINTS

· Across portfolios, we believe the most challenging investment tax issues can often be found in an investor’s fixed income allocation.

· Over time, the right portfolio implementation choices may materially enhance after-tax returns on fixed income investments.

· Over time, the right portfolio implementation choices may materially enhance after-tax returns on fixed income investments.

· Tax-exempt municipal bonds and other tax-advantaged bonds remain a cornerstone of many taxable investors’ fixed income allocation.

· However, for taxable investors who wish to allocate beyond municipals, most asset managers have yet to solve the fixed income tax challenge.

· We believe fixed income investors can reduce tax burdens by focusing on sector and security selection and capital gain/loss management, among other strategies.

A decade of strong market returns combined with recent tax reform has heightened interest in the impact of taxes on investment returns. Taxes are no different from management fees — albeit one essentially levied by governments on investment gains and income. It has been our experience that portfolio implementation choices can materially change the total amount of taxable investment gains and income, as well as the rate at which taxes are paid, in a given year and over the lifetime of an investment. This, in turn, may meaningfully increase or decrease the net returns taxable clients earn on an after-tax basis through time.

Across portfolios, we believe the most challenging investment tax issues can often be found in an investor’s fixed income allocation. Unlike in equity markets, fixed income “buy-and-hold” strategies are generally inefficient from a tax perspective. Indeed, simply holding a bond to maturity typically generates interest or other yield income that may be subject to a 40.8% maximum tax rate on the federal level (and potentially additional state and local taxes). In addition, many actively managed fixed income strategies generate significant short-term gains that are also taxed at the top federal marginal tax rate.

Taking all of this into account, it is not difficult to see how swiftly and deeply taxes can cut into investment returns, especially over a period of years.

Municipal bonds: An important building block

Municipal bonds: An important building block

Given the potentially high tax costs of investing in the fixed income space, many taxable investors choose to buy tax-exempt municipal bonds and/or other similarly tax-advantaged bonds. These types of bonds are a very important building block in any taxable bond portfolio, as they have the distinct advantage of a tax exemption on interest income at the federal level and, at times, the state and local levels as well (dependent on the issuing municipality and other factors). Historically, municipals have played a vital role in many investors’ asset allocation plans, offering not only compelling after-tax income, but also attractive total return and diversification benefits relative to equities as US yields have fallen over the past 30+ years. Higher degrees of correlation between municipal returns and duration (i.e., sensitivity to US interest rates) have been very evident in a downward-trending rate environment.

Taxable fixed income: Not up to the challenge

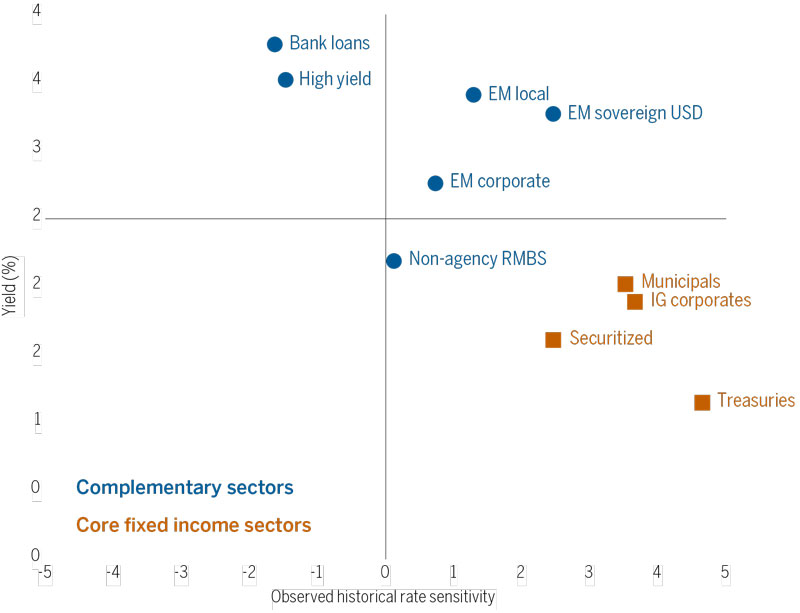

Times are changing. Many fixed income asset classes now offer higher after-tax yields than municipals with less interest-rate sensitivity, along with the potential to outperform municipals in a rate environment characterized by less one-dimensional directionality. In addition, high-profile municipal bankruptcies such as Puerto Rico and Detroit have demonstrated to investors the risk of being overly concentrated in one issuer and/or asset class.

FIGURE 1

Yields and historical rate sensitivity of various fixed income sectors

Source: Wellington Management. All yields besides municipals are calculated on an approximate after-tax basis with an assumed tax rate of 40% as of 31 December 2018. Observed historical rate sensitivity based on 10 years of data through 31 December 2018 | For illustrative purposes only | Yields and observed historical rate sensitivities from the following indices: Wellington Management Non-Agency RMBS Index, CSFB Leveraged Loan Index, Barclays Global High Yield Index, JPMorgan Emerging Markets Bond Index Plus, JPMorgan Govt Bond Index – Emerging Markets Global Div, Barclays Global Aggregate Securitized (a component of the Bloomberg Barclays Global Aggregate Bond Index), Barclays Global Aggregate Corporate (a component of the Bloomberg Barclays Global Aggregate Bond Index) , CG WGBI 1 – 10, JPM CEMBI Broad Index, Bloomberg Barclays 1 – 15 Year Municipal Bond Index. Investments cannot be made directly into an index. PAST RESULTS ARE NOT NECESSARILY INDICATIVE OF FUTURE RESULTS AND AN INVESTMENT CAN LOSE VALUE. While data is believed to be reliable, no assurance is being provided as to its accuracy or completeness.

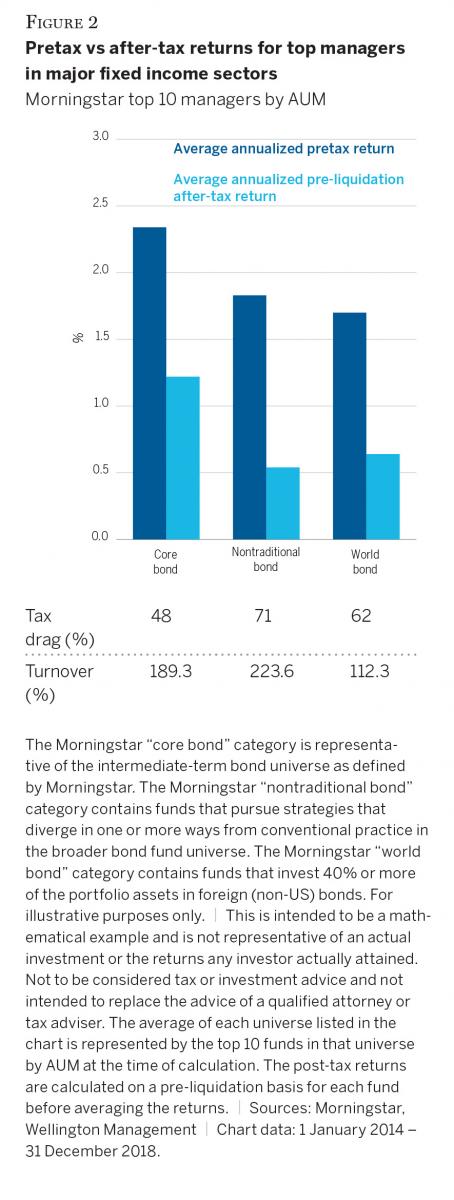

Fixed income investors who want to complement their municipal and cash exposures have several options, including core bond, nontraditional bond, and world bond funds. We believe these segments of the fixed income market may offer distinct benefits: Attractive yields, lower rate sensitivity, opportunity for price dispersion from long-term trends, and greater downside mitigation versus equities are all reasons clients might consider investing in these sectors. In addition, many of the bond funds in these categories have delivered strong pretax total returns.

Fixed income investors who want to complement their municipal and cash exposures have several options, including core bond, nontraditional bond, and world bond funds. We believe these segments of the fixed income market may offer distinct benefits: Attractive yields, lower rate sensitivity, opportunity for price dispersion from long-term trends, and greater downside mitigation versus equities are all reasons clients might consider investing in these sectors. In addition, many of the bond funds in these categories have delivered strong pretax total returns.

The problem for taxable investors is that after-tax returns (pre- and post-liquidation) from taxable bond strategies are often disappointing when compared to pretax returns. The Morningstar database of mutual funds in these categories tells the story: As of 31 December 2018, the average annualized pre-liquidation, after-tax five-year total return generated by the 10 largest funds (by AUM) in each of these categories was under 1.3%, retaining less than half of the pretax total return achieved. Post-liquidation returns (based on a hypothetical liquidation of fund assets) have been simi-larly low, averaging 0.98%.

Why do most taxable fixed income funds deliver so little net return to taxable investors?

We believe typical taxable fixed income funds may carry heavy tax burdens for four reasons:

1. High portfolio turnover rates, triggering substantial short-term capital gains

2. Limited use of tax-loss harvesting to offset taxes on capital gains and income

3. Portfolio manager prioritization of income (yield) over capital gains

4. Structural tax rates associated with most fixed income and many derivative securities, whereby interest and certain derivatives income are taxed at ordinary income rates

The significant tax drag these funds have experienced is a function of their return objectives, which generally are based on a pretax performance target. We believe most asset managers have not yet solved the fixed income challenge for taxable bond investors who wish to allocate beyond municipals.

Food for thought

Fixed income portfolio managers can seek to reduce a bond strategy’s tax burden on investors by focusing on pre-liquidation, after-tax total returns.

We believe achieving better after-tax returns can be realized in two primary ways:

• Sector and security selection across taxable fixed income sectors

• Capital gain/loss management

In doing so, the taxable fixed income investor can seek to access total return, income, and diversification. In our view, such an approach to portfolio man-agement can be an excellent complement to a municipal bond allocation.

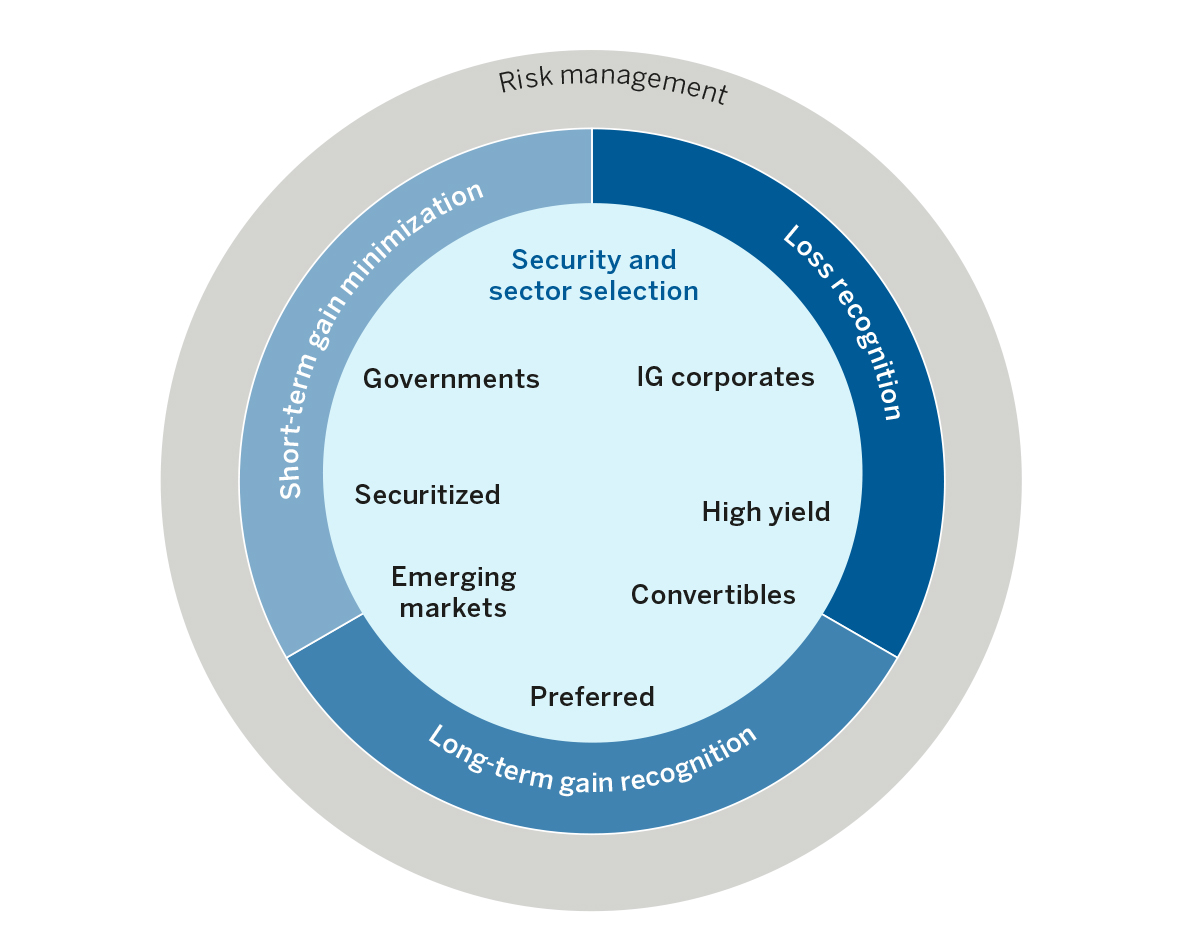

FIGURE 3

Tools for managing taxable fixed income portfolios

Source: Wellington Management. For illustrative purposes only.

Security-level gain and loss management

We believe gain and loss management at the security level, rather than solely at the sector level, creates more opportunities to reduce investors’ tax burden over time. Given this security-level focus, three aspects to gain/loss management are required.

1. Minimize short-term realized gains — With a potential 40.8% tax drag, realizing short-term capital gains can significantly decrease a portfolio’s after-tax total return. According to Morningstar, the average turnover in the Morningstar Total Return Bond category is approximately 200%. In a momentum or positive price environment, turning the portfolio over twice a year results in the “average” manager captur-ing high levels of short-term gains. In our view, minimizing short-term gain realization, attempting to hold most positions for longer than the one-year holding period required to qualify for long-term capital gains treatment (subject to a tax rate of 23.8%) is the first line of defense.

1. Minimize short-term realized gains — With a potential 40.8% tax drag, realizing short-term capital gains can significantly decrease a portfolio’s after-tax total return. According to Morningstar, the average turnover in the Morningstar Total Return Bond category is approximately 200%. In a momentum or positive price environment, turning the portfolio over twice a year results in the “average” manager captur-ing high levels of short-term gains. In our view, minimizing short-term gain realization, attempting to hold most positions for longer than the one-year holding period required to qualify for long-term capital gains treatment (subject to a tax rate of 23.8%) is the first line of defense.

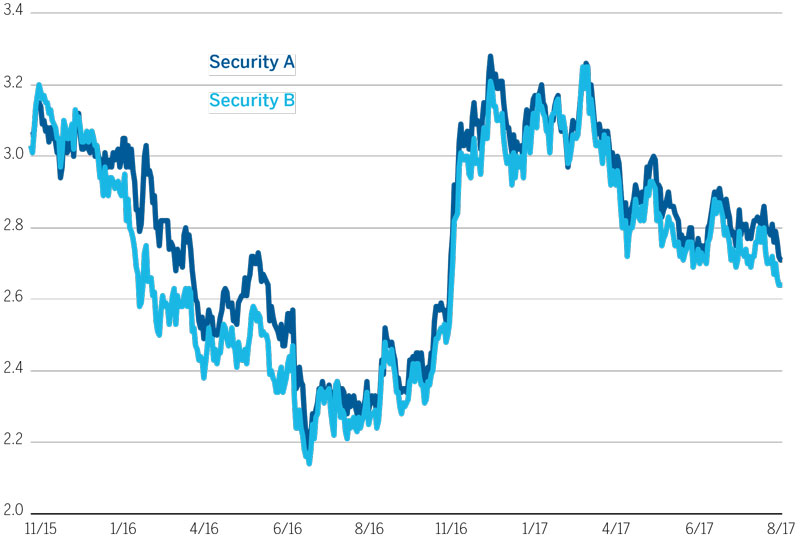

2. Realize short-term losses — As any taxable investor knows, capital losses can be very beneficial to a portfolio manager in that they off-set realized capital gains. In the equity context, “tax-loss harvesting” strategies are common. Selling and then staying out of loss-generating securities for 30 days (to avoid the “wash sale” rules that can defer rec-ognition of realized losses) is the cornerstone of tax planning in equity markets. In fixed income, tax-loss harvesting is usually easier than in the equity space because different bonds may trade similarly, whereas different equities often diverge in value significantly, even where the issuers are in the same industry. FIGURE 4 shows the yield differential between two hypothetical bonds (“Security A” and “Security B”): Holders of bonds can often experience little difference in return and volatility exposure, despite the two companies having differing products and earnings outlooks. Rotating out of securities that have produced losses and into securities with similar (but not identical) return profiles may preserve similar economic exposure while creating an important tax asset.

3. Actively realize some long-term gains — Given the dominance of coupon income as a return driver in fixed income, combined with higher tax rates on this component of return, there is an explicit trade-off between “clipping” the coupon and pulling forward returns in the form of long-term capital gains. Realizing long-term gains may increase your initial tax burden, but it may lower your future tax bill if you invest in the same security. A fixed-life security with an approaching termination date (like a bond), which has accrued some long-term capital gain, will generally have a lower yield than when it was initially purchased. By realizing long-term gains, the investor is paying the lower long-term capital gains rate and reducing future ordinary income (since the bond is at a lower yield), which is taxed as high as 40.8%.

3. Actively realize some long-term gains — Given the dominance of coupon income as a return driver in fixed income, combined with higher tax rates on this component of return, there is an explicit trade-off between “clipping” the coupon and pulling forward returns in the form of long-term capital gains. Realizing long-term gains may increase your initial tax burden, but it may lower your future tax bill if you invest in the same security. A fixed-life security with an approaching termination date (like a bond), which has accrued some long-term capital gain, will generally have a lower yield than when it was initially purchased. By realizing long-term gains, the investor is paying the lower long-term capital gains rate and reducing future ordinary income (since the bond is at a lower yield), which is taxed as high as 40.8%.

FIGURE 4

Yield-to-maturity differential: “Security A” vs “Security B”

For illustrative purposes only. | This is intended to be a mathematical example and is not represen-tative of an actual investment or the returns any investor actually attained. Not to be considered tax or investment advice and not intended to replace the advice of a qualified attorney or tax adviser. The use of alternative assumptions, including trade dates, tax rates, yield levels, and price levels, would produce different results. The assumptions made include: For security A, purchase date of 1 December 2015, sell date of 20 December 2016, yield of 2.82% as of purchase date; for security B, purchase date of 20 December 2016 and yield of 3.14% as of purchase date. Additional assumptions include similar expire dates and coupon rates and a tax rate of 37%. | Sources: Bloomberg, Wellington Management. | Chart data: 1 November 2015 – 31 August 2017. Wellington has reviewed the above research and believes the findings are still valid even with the inclusion of more recent data.

For most fixed income investments, we believe investors are better off realizing long-term gains than paying higher ordinary income tax rates. As such, the “payback” period of this initial tax liability could be many years.

For bonds where the breakeven period is less than two years, we believe it may make sense to realize these long-term gains to reduce future ordinary income (and therefore taxes) for clients.

The bottom line

The bottom line

We believe tax management of fixed income should be at the forefront of investors’ minds, given the substantial tax drag often associated with these holdings. Moreover, we believe taxable bond portfolios, managed with the taxable investor in mind, can be a diversifying agent to municipal bond allocations, given their reliance on duration to provide attractive levels of yield and the concentrated opportunity set for these bonds.

Important disclosure

For informational purposes only and should not be viewed as an offer to sell or the solicitation to buy securities or adopt any investment strategy. Views expressed reflect the current views of the authors at the time of writing, are based on available information and subject to change without notice, and should not be taken as a recommendation or advice. Individual portfolio management teams may hold different views and may make different investment decisions for different clients. The information presented in this material has been developed internally and/or obtained from sources believed to be reliable; however, Wellington Management does not guarantee the accuracy, adequacy, or completeness of such information.

-Edit_M_V2.jpg "Chris Goolgasian, cfA, cpA, cAiA Director of Climate Research and Portfolio Manager") This document may contain certain statements deemed to be for-ward-looking statements. All statements, other than historical facts, contained within this document that address activities, events, or developments that the authors expect, believe, or anticipate will or may occur in the future are forward-looking statements. These statements are based on certain assumptions and analyses made by the authors in light of their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are appropriate in the circumstances, many of which are detailed herein. Such statements are subject to a number of assumptions, risks, and uncertainties, many of which are beyond Wellington Management’s control. Please note that any such statements are not guarantees of any future performance and that actual results or developments may differ materially from those projected in the forward-looking statements.

This document may contain certain statements deemed to be for-ward-looking statements. All statements, other than historical facts, contained within this document that address activities, events, or developments that the authors expect, believe, or anticipate will or may occur in the future are forward-looking statements. These statements are based on certain assumptions and analyses made by the authors in light of their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are appropriate in the circumstances, many of which are detailed herein. Such statements are subject to a number of assumptions, risks, and uncertainties, many of which are beyond Wellington Management’s control. Please note that any such statements are not guarantees of any future performance and that actual results or developments may differ materially from those projected in the forward-looking statements.

The indices referenced herein are broad-based securities market indices and are used for illustrative purposes only. Broad-based securities indices are unmanaged and are not subject to fees and expenses typically associated with managed accounts or investment funds. Investments cannot be made directly into an index.

Risks

Below-investment-grade – lower-rated or unrated securities may have a significantly greater risk of default than investment-grade securities, can be more volatile, less liquid, and involve higher transaction costs.

Capital – investment markets are subject to economic, regulatory, market sentiment, and political risks. All investors should consider the risks that may impact their capital before investing. The value of your investment may become worth more or less than at the time of the original investment may experience high volatility from time to time.

Concentration – concentration of investments within securities, sectors or industries, or geographical regions may impact performance.

Credit – the value of a bond may decline, or the issuer/guarantor may fail to meet payment obligations. Typically, lower-rated bonds carry a greater degree of credit risk than higher-rated bonds.

Currency – the value of investments may be affected by changes in currency exchange rates. Unhedged currency risk may subject investments to significant volatility.

Derivatives – derivatives may provide more market exposure than the money paid or deposited when the transaction is entered into (sometimes referred to as leverage). Market movements can therefore result in a loss exceeding the original amount invested. Derivatives may be difficult to value. Derivatives may also be used for efficient risk and portfolio management, but there may be some mismatch in exposure when derivatives are used as hedges. The use of derivatives forms an important part of the investment strategy.

Derivatives – derivatives may provide more market exposure than the money paid or deposited when the transaction is entered into (sometimes referred to as leverage). Market movements can therefore result in a loss exceeding the original amount invested. Derivatives may be difficult to value. Derivatives may also be used for efficient risk and portfolio management, but there may be some mismatch in exposure when derivatives are used as hedges. The use of derivatives forms an important part of the investment strategy.

Leverage – the use of leverage can provide more market exposure than the money paid or deposited when the transaction is entered into. Losses may therefore exceed the original amount invested.

Emerging markets – emerging markets may be subject to custodial and political risks and volatility. Investment in foreign currency entails exchange risks.

Hedging – any hedging strategy using derivatives may not achieve a perfect hedge.

Interest rates – the value of bonds tends to decline as interest rates rise. The change in value is greater for longer-term than shorter-term bonds.

Manager – investment performance depends on the investment management team and its investment strategies. If the strategies do not perform as expected, if opportunities to implement them do not arise, or if the team does not implement its investment strategies successfully, investments may underperform or experience losses.

Short selling – a short sale exposes investments to the risk of an increase in the market price of a security sold short; this could result in a theoretically unlimited loss.

Visit Wellington Management for more information and contact details.