The tide of liquidity is turning faster than many investors anticipate

It is hard to overstate how far free and unlimited central bank liquidity has rewired the financial system. As central bankers extract themselves from the monetary rabbit hole they have burrowed their way into, the damage to traditional portfolios is likely to be considerable.

This tightening of monetary policy is happening because inflation has returned – with a vengeance. Central banks are lifting short-term interest rates at a brisk pace. But there is an additional danger for liquidation-prone markets: quantitative tightening (QT).

The major central banks are now shrinking their balance sheets – the US Federal Reserve (the Fed) by $95 billion per month from this September. Private investors will have to absorb a lot more duration risk than they have recently been doing, the net result being higher long-term interest rates.

In markets hard-wired to a belief in ‘low for long’ interest rates, it is no surprise risk assets have been hit. But there is another reason: by shrinking its balance sheet, the Fed’s QT will drain liquidity from the banking system.

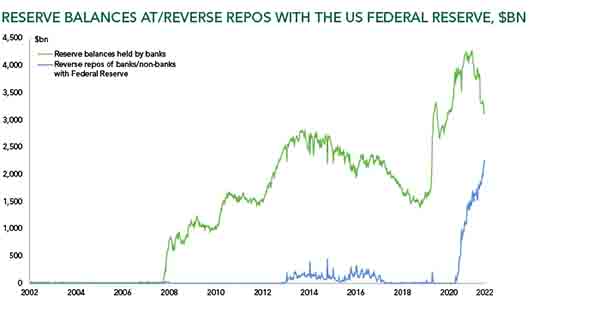

This may not matter initially: commercial bank reserves at the Fed are still north of $3 trillion. But they are already falling fast and may soon reach a biting point where dealers’ liquidity-providing role becomes impaired. We hit just such a biting point in the second half of 2018. Back then inflationary dangers were absent and the Fed could reverse course abruptly. This time around, the Fed has no choice but to keep its foot on the brake.

No one knows where this biting point actually is, not even the Fed. Four years ago, it underestimated the dramatically higher level of reserves banks wanted to operate with, given the much tighter regulatory environment. Today, the Fed is still in the dark.

Worse, another force is acting to drain bank liquidity – ironically, a creation of the Fed itself. The ‘reverse repo’ facility (RRP) allows intermediaries to place funds overnight at the Fed, secured against US Treasury collateral. This otherwise innocuous corner of the payments architecture is important because it provides access to the Fed’s balance sheet for non-banks, specifically the $4.5 trillion money market mutual fund (MMMF) industry. Over $2.2 trillion of funds are now parked at the Fed each evening via the RRP, the vast bulk of which comes from the MMMF sector.

MMMFs’ use of the RRP drains reserves out of the banking system, dollar for dollar. In short, it gets us to the liquidity biting point faster than QT alone. How much faster is uncertain, but demand for RRP access is growing (see chart) – and likely to keep on doing so. When interest rates are rising, cash investors switch into MMMFs because they increase their rates faster than the banks, making them more attractive. And as funds invested in MMMFs grow, so will the desire to place those funds in the Fed’s RRP.

This dynamic could matter a lot over the next six to 12 months. In 2018, we learnt that a shortage of bank reserves can trigger financial dislocation. In 2022-2023, given the Fed’s single-minded pursuit of tight money, we may discover just how damaging and pervasive such dislocation can be in markets that have been pumped up by more than a decade of monetary largesse. As Warren Buffet observed, it is only when the tide goes out do you discover who is swimming naked. The impending liquidity drain, many assets - and indeed investors - may soon be exposed.

Sources: US Federal Reserve

Past performance is not a guide to future performance. The value of investments and the income derived therefrom can decrease as well as increase and you may not get back the full amount originally invested. Ruffer performance is shown after deduction of all fees and management charges, and on the basis of income being reinvested. The value of overseas investments will be influenced by the rate of exchange.

The views expressed in this article are not intended as an offer or solicitation for the purchase or sale of any investment or financial instrument, including interests in any of Ruffer’s funds. The information contained in the article is fact based and does not constitute investment research, investment advice or a personal recommendation, and should not be used as the basis for any investment decision. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. This document does not take account of any potential investor’s investment objectives, particular needs or financial situation. This document reflects Ruffer’s opinions at the date of publication only, the opinions are subject to change without notice and Ruffer shall bear no responsibility for the opinions offered. Read the full disclaimer.