Still open for families: Family offices take on the Brexit challenge

Britain has taken the first step down a long and uncertain road to its departure from the European Union. James Beech asks financial experts if family offices are in for a bumpy ride

More than 17 million Britons voted on 23 June to leave the European Union after 43 years – triggering a tsunami of unprecedented political upheaval and volatility in financial markets which has shaken the United Kingdom and reverberated around the world.

Prophecies of economic doom, unheeded by the majority of Britons who voted to exit, have started to come true.

The International Monetary Fund (IMF) expects the UK economy to grow by 1.3% in 2017, 0.9 points lower than estimated in its world economic outlook in April. The IMF declared that Brexit has “thrown a spanner in the works” in the fragile global recovery despite stronger than forecasted growth in the eurozone and Japan, and an upturn in commodity prices.

But are family offices frightened by the doomsayer's dire predictions? Is this the beginning of the end? Or the end of the beginning?

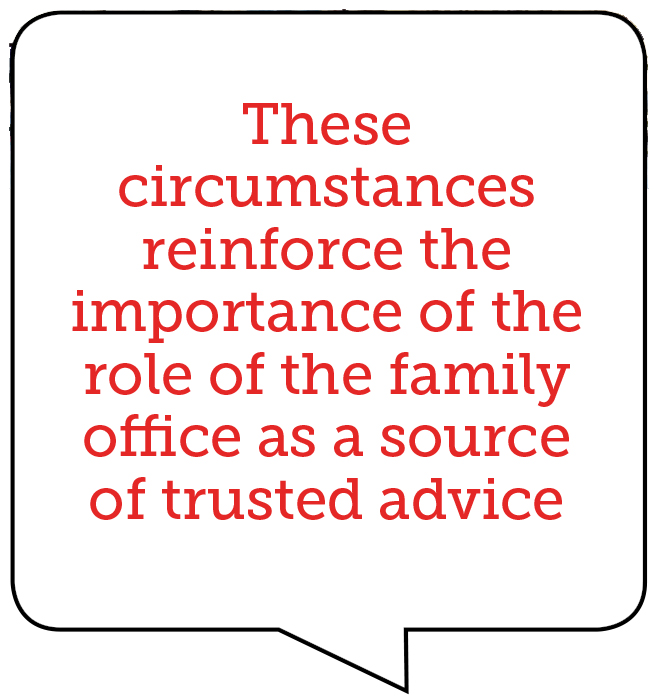

Family offices, their advisers, and wealth managers are not immune from uncertainty but as Anton Sternberg, investments chief executive at multi family office Stonehage Fleming, says, “these circumstances reinforce the importance of the role of the family office as a source of trusted advice. In times of change and uncertainty, families need wise counsel.”

Consultancy KPMG's initial advice is for family office clients to review their operations and get a clearer picture of their potential exposure, but to avoid any knee-jerk reactions.

“We are working with [clients] to help them formulate their response to Brexit, and the short, medium, and long-term actions that might follow in what we are calling the 2:2:2 plan - '2 weeks, 2 months, 2 years',” Catherine Grum, head of family office services, explains.

A good way to plan is to use the framework of the EU's four freedoms – goods, capital, people, and services – in the immediate and long term.

“From the perspective of a family office, the key questions are: do they have any employees or family members living in the UK who are EU nationals, or UK nationals working elsewhere in the EU?

“What capital do they have in the UK and elsewhere in Europe? What cross-border services are they using? Other issues such as tax implications will come later as negotiations commence and we have more clarity on the direction of travel.”

European family offices are concerned about the impacts of Brexit on the value of sterling investments, specifically real estate, says Philip Higson, vice chairman at UBS Global Family Office group in Zürich.

Real estate is illiquid and needs a longer process for concluding purchase or sale.

However, Higson says Brexit is less of an issue for single family offices in London because they do not sell or operate in multi-jurisdictional Europe and do not need to be linked to the continent, though other issues will affect them.

Oliver Williams, head of WealthInsight – which publishes data on wealthy individuals and families – notes that many high net worth individuals (HNWIs) are counting the cost after the Brexit vote.

“With the majority of HNWIs in the UK (14.3%) owing their wealth to the financial services industry, the billions that have been wiped off markets recently would have directly hurt the pockets of many HNWIs.” Williams says.

“The billionaire champions of Brexit, Sir Anthony Bamford and James Dyson, may both see a rise in their fortunes as a weak sterling favours manufacturers.

“Other HNWIs involved in exporting could benefit from this imminent currency uncertainty,” he adds.

Dismay was not limited to British shores. Brexit will “most certainly” deter US family offices from investing in London or the UK, believes Timothy Lappen, a partner at major Los Angeles-based law firm, Jeffer Mangels Butler & Mitchell LLP, and founder and chairman of the LA-based Family Office Group and the Luxury Home Group.

US clients tell Lappen that Brexit “makes no sense for England or the EU” and they hope Parliament will not proceed with the departure.

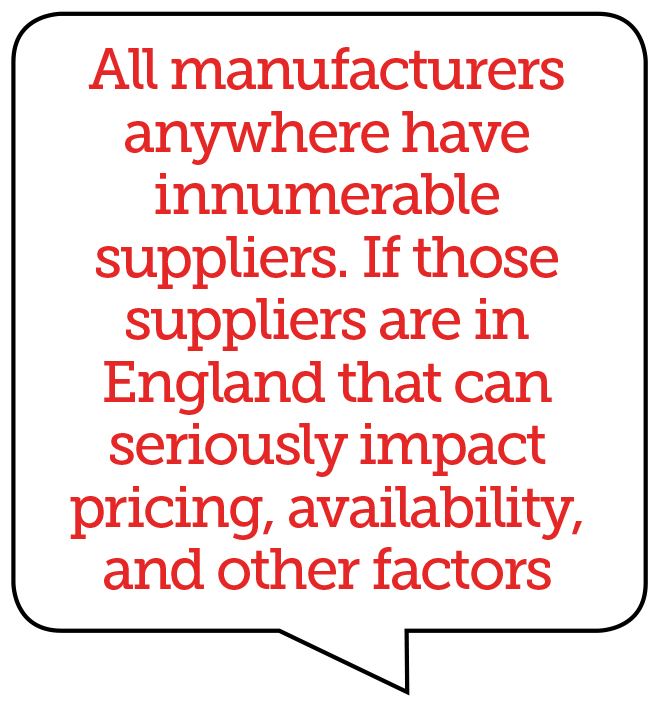

He says while everyone likes a bargain, “uncertainty will impact investors even more. Some, of course, have such exposure already. For example, they could be invested in a US company which has major relationships. A great example of these issues is the auto industry.

He says while everyone likes a bargain, “uncertainty will impact investors even more. Some, of course, have such exposure already. For example, they could be invested in a US company which has major relationships. A great example of these issues is the auto industry.

“All manufacturers anywhere have innumerable suppliers. If those suppliers are in England that can seriously impact pricing, availability, and other factors,” Lappen concludes.

"With the uncertainty surrounding Brexit, I would expect to see additional investments in American businesses and real estate, including luxury homes. Investments in the United States are an excellent “asset class” for a well-diversified portfolio."

WATERLOO SUNSET?

Other market watchers disagree with Lappen and remain confident London will not lose its lustre of appeal among the wealthy around the world, whatever the outcome of Britain's negotiation with the EU.

Britain is home to 26 Fortune Global 500 companies with 17 of them based in London, while Point72 Asset Management – the $11 billion family office of Steve Cohen and employees – has doubled the size of its London office in the past six weeks, the NY Times reported.

The capital has more ultra-HNWIs than any other city in the world, Williams at WealthInsight observes.

“London's superior education standards and quality of life will continue to be a bigger draw for migrating HNWIs over its financial markets,” he adds.

Jon Needham, head of fiduciary services at Societe Generale Private Banking (SGPB) and SGPB Hambros, believes principals might actually find London more attractive in the longer term as their base for family office activities. Brexit does not necessarily mean loss of access to the single market, he claims.

Jon Needham, head of fiduciary services at Societe Generale Private Banking (SGPB) and SGPB Hambros, believes principals might actually find London more attractive in the longer term as their base for family office activities. Brexit does not necessarily mean loss of access to the single market, he claims.

More than two years of events, negotiations, and decisions have to pass before anyone can judge if London's status as a financial hub and as a focal point for wealthy international families is likely to be challenged, Sternberg declares.

“It is also not clear yet the extent to which Brexit will produce fault lines elsewhere in the EU which may ultimately be to London's benefit and, in the immediate aftermath of the vote, the fall in the value of sterling increases London's competitiveness as an operational and residential centre,” says Sternberg.

Savills, a UK-based real estate agency, expects the majority of leasing markets will return to normal in the medium term.

“The exception to this will be the banking and financial services sectors, where questions over passporting and the Alternative Investment Fund Managers Directive will linger,” Mat Oakley, head of commercial research at Savills, says.

HSBC and Barclays, two of the UK's largest banks, have pledged to keep their London headquarters. Yet Standard Chartered is ready to move its headquarters out of the City of London if Brexit prompts politicians to saddle the banking sector with more taxes.

Jonathan Bell, chief investment officer at Stanhope Capital, says Brexit would make “absolutely no difference” for single family offices when choosing London as their headquarters.

Most multi family offices will still want to be based in Geneva or London, or maybe Zurich, and ease of cross-channel travel is not going to change, Bell notes. But there was an implication for any multi family office that wants to market in Europe if the UK loses its passport right, he adds.

“If we lose the passport, you either do what Swiss bankers have done for years, which is visit clients in Paris and say you are just talking socially for lunch, the banks don't take any documents and wait for [the clients] to come to you. I think London would still remain a key hub and clients would come to them.

“Or you say we need an office within the EU with a passport to be able to sell across the EU and that is something we would consider if it came to it. I do not think it will come to it but it is something we will have to consider,” he cautions.

RULES AND REGULATIONS

Family offices may decide to pause some of their inward investment plans as a consequence of Brexit. However, with sterling now relatively cheap, compared to pre-Brexit vote levels, some see good investment opportunities, Needham says.

UBS's Higson believes there would be a question mark over the ability of regulated multi family offices in London to work with families from non-UK jurisdictions.

UBS's Higson believes there would be a question mark over the ability of regulated multi family offices in London to work with families from non-UK jurisdictions.

“The regulation which is stressing people – and it is more for the fund distributors in multi family offices, the fund distribution agreement they may have, or the ability to have a contractual relationship with somebody outside the UK – will be subject to a new regime potentially, so they would be worried.”

Higson notes most family offices are in London because their customers are in London, and their customers are in London because the tax regime in the capital is better than it is in much of continental Europe.

“In the event the Brexit debate causes a change in the residential non-domiciled status or a change in corporate tax in the UK, your competitor locations are Monaco, Luxembourg, and Switzerland because all substantial family offices spend a large amount of time trying to make sure they are correctly located in terms of tax,” says Higson.

A recent survey of 115 non-domiciled residents suggests 37% are considering leaving the UK permanently with almost two-thirds (64%) citing changes to their tax status as a key reason for considering a move, according to UK accountancy firm Moore Stephens.

“Nobody is rushing to go from London to Paris, Frankfurt, or Vienna or anywhere else because there is no point,” says Higson, although he expects there to be uncertainty around the positioning of Luxembourg, post-Brexit, as many fund structures were based in the EU city.

“Nobody is rushing to go from London to Paris, Frankfurt, or Vienna or anywhere else because there is no point,” says Higson, although he expects there to be uncertainty around the positioning of Luxembourg, post-Brexit, as many fund structures were based in the EU city.

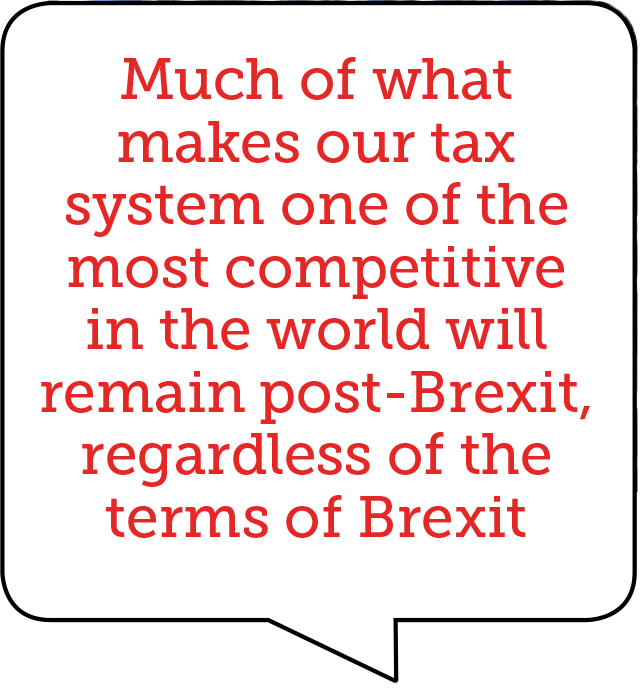

Elizabeth Bradley, partner and head of corporate tax at Berwin Leighton Paisner, warns Brexit will have a “significant effect” on the UK tax system in the medium term.

“However, much of what makes our tax system one of the most competitive in the world will remain post-Brexit, regardless of the terms of Brexit.

“We will retain a substantial tax treaty network, a generous exemption from tax on dividends, one of the lowest corporation tax rates in Europe and, for now at least, generous tax deductions for interest.

“Although some of these benefits may change if the public finances worsen, they are generally within our control and any future government would be wise to retain them to preserve our competitiveness.”

If Britain leaves the EU and opts for “the Norway option” by becoming one of the member states of the European Economic Area (EEA), the UK will be required to adopt and comply with EU financial services legislation but, crucially will have no means of participating in the making of the legislation.

“If we leave the EU and also do not opt for EEA membership, we will be a 'third country and access to EEA markets will be restricted,” Victoria Younghusband, partner at Charles Russell Speechlys, says.

“Some may suggest this is of benefit to the financial services community, as we can avoid the prescriptive detail and the frustrations of European financial services legislation, which is often an unnecessary and expensive overlay on a well-functioning UK capital market,” Younghusband adds.

SILVER LINING

Several commentators are looking at the bright side of Brexit, now the shock of the referendum result has subsided. Some call on the new government to make London and the UK more attractive for family offices.

“There could be a rediscussion around the resident non-domiciled status and domicile rules which were brought up in the Osborne budget of 2015 which are due to go into effect in 2017,” Higson says.

“A family office did say there was a chance that might be reviewed or delayed given what is happening. There could be a silver lining in that the government, whomever it might be, reconsiders other choices they have got with respect to the UK as a destination for inward investment, which obviously includes family offices,” Higson adds.

“A family office did say there was a chance that might be reviewed or delayed given what is happening. There could be a silver lining in that the government, whomever it might be, reconsiders other choices they have got with respect to the UK as a destination for inward investment, which obviously includes family offices,” Higson adds.

For many family offices, UK real estate is a cornerstone investment and with the weaker sterling there could be opportunities for international family offices to make acquisitions.

“With instability and uncertainty across Europe and also the US with the forthcoming elections, care needs to be taken not to jump out of the frying pan and into the fire, when considering switching to assets in alternative markets,” Grum at KPMG advises.

The sudden initial drop off in the FTSE 100 as investors reacted to the referendum result presented good buying opportunities for investors.

Richard Potts, partner at Irwin Mitchell Asset Management, considers the fall in the value of sterling a benefit for companies with large overseas earnings.

“As many of these companies are large and overseas earnings represent a significant proportion of companies in the FTSE, this boost to earnings could attract buyers,” Potts adds.

“As many of these companies are large and overseas earnings represent a significant proportion of companies in the FTSE, this boost to earnings could attract buyers,” Potts adds.

“Coupled with this is that the economic implications of Leave will take many years to unfold.

“Bond markets are likely to rally further as investors seek safe haven assets during a period of uncertainty. It is possible that longer dated bonds will not prosper in the longer term as weaker sterling translates into higher inflation and foreign investors who typically buy longer bonds desert all UK markets.”

Williams at WealthInsight believes deregulation could benefit personal wealth.

“The bonus-cap may be one of the more symbolic pieces of regulation imposed on the City of London from Brussels. However, as other areas of financial services – mostly niche and boutique firms – are alleviated from EU regulation, they could start to prosper.

“Rarely has proper financial planning and risk management been in more demand. Many HNWIs will therefore seek out private banks to manage their portfolio, instead of relying on a do-it-yourself or FinTech approach,” says Williams.

While Stonehage Fleming is still assessing the implications of the vote on its medium to long-term expectations of investments, early results had been “encouraging,” Sternberg observes.

“Our sterling portfolios have a strong global orientation, equity allocations in general emphasise more resilient defensive stocks, and we have very little exposure to financials which have been volatile.

“We have also had positive returns from a number of our alternatives managers. Despite extraordinary political drama, we are reassured that markets at least have behaved in a largely rational and orderly manner.”

Needham at SGPB sums up the situation facing family offices dealing with a Brexit world.

“Today there are so many unknowns it is impossible to act with certainty. As a consequence we should all focus on what we do know and not allow the 'what ifs' to distract us,” he concludes.

“If we allow ourselves to become too distracted with these 'unknowns' we will expend time, money, and resources unnecessarily and likely fruitlessly. Concentrating on the 'knowns' brings a degree of certainty to the decision-making process and provides a better foundation for rational decision making.”