Investors need to look beyond the conventional for real returns

In the Back To The Future trilogy, the bad guy is a bully called Biff Tannen.

The megalomaniac mogul amassed his wealth because his older self travelled back in time to give his younger self the Grays Sports Almanac, a compilation of every sports result from 1950 to 2000. So Biff was able to earn a spectacular fortune from sports betting.

Financial markets – with their twists and turns and unknowability – remind us just how hard it is to predict the future and just how wonderful perfect foresight would be.

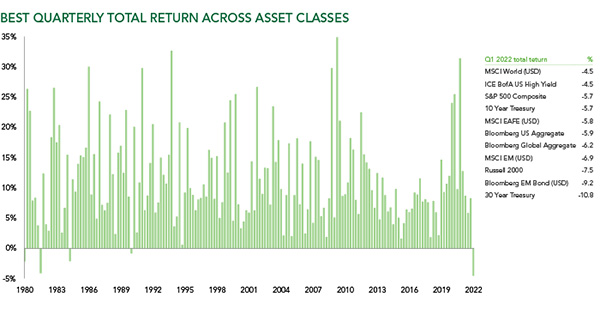

This month’s chart shows the returns you could have earned across global stocks and bonds if you had had that crystal ball and could have picked exactly the best place to be invested each quarter. Over the decade to the end of 2021, you would have delivered a 35x return on your original investment. Looking further back, if you had started in 1980 with a portfolio of £100,000, this would have compounded to £4.8 billion by the end of last year.

Yet, in the first quarter of 2022, even Biff would have been bashed.

The best case scenario for stock and bond investors was a -4.5% return from high-yield bonds. Everything else was worse. Equities, sovereign bonds, corporate bonds, infrastructure, property, private equity, private credit, venture capital and cryptocurrencies all posted negative returns. There was nowhere to hide – and that is before adjusting for the 7% inflation ravaging your capital.

We have called this the illusion of diversification. The balanced portfolio was not balanced. The assets investors believed to be diversifiers turned out to have higher cross-asset correlations than first thought. They all appear vulnerable to the same risks – rising interest rates and rising risk premiums, which both appear to be happening at the same time. The only place to hide in conventional assets was commodities.

In the 165 quarters since 1980, only five markets have been so dismal even Mystic Meg couldn’t have conjured a positive return. For the last time this happened, we must travel back to 1990. The scary thing for investors is that the current quarter appears to be offering more of the same. In April, the Nasdaq had its worst monthly performance since 2008, falling 13.3%. Bonds fared little better – the Bloomberg Global Aggregate index, a broad-based fixed income benchmark, fell 5.5% over the month. In a crisis, all correlations go to one.

At Ruffer, we have long been warning that we may be going to go back to the future once more. We expect the coming decade to have similarities to the 1970s – a period of political, economic and inflationary turmoil – with all the market volatility investors rightly dread. Unfortunately, this time nobody has Grays Stockmarket Almanac to guide them through the mayhem.

At times, investors may once again feel like there really is nowhere to hide. To preserve capital, they will require a new approach to constructing portfolios – flexible, adaptable, robust and responsive. Being unbenchmarked and unconventional could prove crucial.

The views expressed in this article are not intended as an offer or solicitation for the purchase or sale of any investment or financial instrument, including interests in any of Ruffer’s funds. The information contained in the article is fact based and does not constitute investment research, investment advice or a personal recommendation, and should not be used as the basis for any investment decision. This document does not take account of any potential investor’s investment objectives, particular needs or financial situation. This document reflects Ruffer’s opinions at the date of publication only, the opinions are subject to change without notice and Ruffer shall bear no responsibility for the opinions offered. This financial promotion is issued by Ruffer LLP. Read the full disclaimer.