Fundraising – will less market froth create more investment discipline?

With nearly $12 trillion raised, the decade leading up to 2022 was truly remarkable for growth in private capital fundraising [1]. But since then the pace of growth has slowed considerably, leaving us amid the most competitive market for new capital since the last global financial crisis (GFC), say Titanbay.

Global consultancy firm Bain & Company recently estimated that the total amount of capital raised in private market strategies over 2023 will be 28% lower than in 2022. Although Bain expects the total for this year to exceed $1 trillion, this would represent the lowest yearly amount since 2015. It would also be a significant reduction compared to the record fundraising activity in the post-Covid boom years of 2021 and 2022 [2].

The same report cites figures from research-firm Preqin stating that nearly 14,000 private capital funds are pursuing $3.3 trillion across various asset classes. If this is the case, around 70% of the available allocation could go unfilled in 2023.

While all of this points to a reduction in the amount of capital available to general partners (GPs), there is some cause for optimism as a reduction in market froth could result in a more grounded and disciplined investment landscape.

What’s behind the slowdown?

Several headwinds have combined to make limited partners (LPs) much more cautious about committing capital, putting a brake on private capital fundraising.

A challenging macro background

Ongoing macroeconomic uncertainty is one of the strongest. It has been driven by a range of causes over the past 18 months. Turbulence in the banking sector and major geopolitical stresses – such as Russia’s war in Ukraine – are well-documented examples that have driven supply-chain disruption and spiking inflation.

Central banks, initially cautious about overreacting with their responses, have now shifted to a hawkish approach with aggressive interest rate increases. Over the same period, in the fastest interest-rate hiking cycle in US history, the Federal Reserve upped the US base rate by more than five percentage points from its previous near-zero level. By the end of July 2023, the effective federal funds rate stood at its highest point in 22 years, a range between 5.25% and 5.5% [3]. The Bank of England and European Central Bank have followed similar paths, though at a relatively slower pace.

Additionally, the early months of 2023 brought some of the highest levels of instability in the banking sector since the GFC. Silicon Valley Bank, First Republic Bank and Credit Suisse collapsed due to a combination of idiosyncratic issues and an escalating crisis of confidence. While the Federal Reserve and other governing bodies took measures to return stability to financial markets, the potential for further volatility persists, making the outlook less clear.

An imbalance in LPs' portfolios

Another headwind is the “on-paper” overweighting in LPs’ portfolios towards private markets. Known as the denominator effect, it arises when one part of a portfolio falls sharply in value, with the result that the remaining parts now constitute a higher proportion of the total value. According to Bain, one-in-three LPs is currently over-allocated to private equity [2].

With listed company valuations falling in 2022, as a result of declines and volatility on public markets, many LP portfolios now have a transient imbalance, being overweight towards private markets. While public market indices are now showing signs of cautious optimism, remaining broadly flat or rebounding over the year to date, pension funds and insurance companies still have strict limits on how much of their portfolios can be allocated to less liquid assets. As such, they are particularly susceptible to the denominator effect.

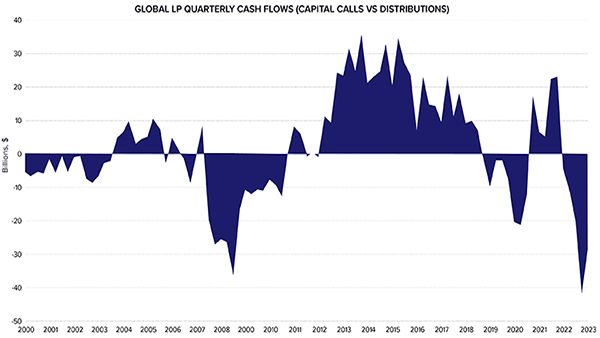

Additionally, the dual challenges presented by macroeconomic conditions and a largely closed IPO window are creating a difficult exit environment for GPs. Many funds are now postponing their portfolio company deal exit strategies until more favourable conditions emerge. Bain says that buyout funds are sitting on a record $2.8 trillion in unrealised assets, over four times the amount held during the GFC [2]. Slow distributions have led to negative LP cash flow, with capital calls from GPs significantly exceeding fund distributions in recent quarters. In turn, this lower liquidity has reduced LPs’ appetite for new commitments.

For GPs, demand will exceed supply

Alternative asset managers are seeking to sustain double-digit fundraising growth, but Bain’s report predicts that institutional capital allocated to private markets will grow at only 8% per year over the next decade. Such a shortfall is likely to further intensify competition for traditional funding sources.

In the near term, we expect large institutional investors to continue to provide the majority of the capital raised by private equity funds, but we also believe that wealth management channels and individual investors will grow their exposure to private markets more rapidly. Boston Capital Group (BCG) predicts these investors will increase their exposures to private equity at a compound annual growth rate (CAGR) of 18.8% [4]. In the same report, BCG says that by 2025, individuals will supply 10.6% of the total capital raised by private equity funds and that they will have 2.4x more AUM in private equity funds than they had in 2020.

This illustrates a rapidly growing market that will provide a progressively vital source of funding for private equity managers as they seek to bridge the demand gap.

Reasons for optimism…

1. Market froth will be removed

In this context, froth refers to recent years’ market exuberance and buoyant valuations, resulting from the abundance of capital seeking investment opportunities. In a more challenging environment of slower fundraising and capital that is less readily available to GPs, we could see a more grounded and disciplined investment landscape.

First, with a reduced amount of capital available to deploy, and the resultant reduced pressure to deploy it quickly, GPs typically become more discerning and diligent in their investment selection process.

Second, in a less frothy environment, GPs are less likely to underwrite deals against inflated valuations.

Third, in a more competitive fundraising environment, GPs may increase their focus on the performance of existing funds. By doing so, they hope to attract new investors and encourage re-ups, as well as taking a more patient approach to adding value to portfolio companies over an extended period.

2. GPs are exploring innovative cash distribution methods

GPs are now more commonly distributing capital to LPs via continuation vehicles and partial sales of portfolio companies. Some have considered other liquidity solutions too, such as purchasing stakes in their own funds from existing investors. LPs can then recycle the proceeds as commitments to new funds. By proactively providing liquidity solutions to LPs in this difficult environment, GPs can strengthen investor confidence for future commitments to the asset class.

3. Fundraising models are evolving and alternative capital sources are gaining traction

In this challenging fundraising environment, GPs have been returning to the market more slowly and fundraising for longer. For some, the push to achieve a well-diversified LP base has become a higher priority. These GPs are replacing traditional approaches by adapting, scaling and tailoring their fundraising functions appropriately. By being better positioned to target a broader range of clients, they will be better positioned to capture new capital.

Additionally, GPs are exploring new paths to growth with individual investors representing an important source of future fundraising. Alternative asset managers are targeting retail capital using a range of commercial and sales strategies, and some are taking more than one approach.

What does this mean for the future?

Already, GPs are demonstrating greater discipline and are holding themselves to a higher bar when underwriting investments. While the era of cheap capital and easy returns has ended, it’s likely that a private equity model based not on financial engineering, but rather on effecting real change, can still be expected to thrive.

Endnotes

1. 2022 Annual Global Private Market Fundraising Report, Pitchbook

2. Taking Private Equity Fund-Raising to the Next Level | Bain & Company, July 2023.

3. Fed raises interest rates to highest in 22 years - BBC News

4. The Future Is Private: Unlocking the Art of Private Equity in Wealth Management, BCG March 2022.

Important disclosures

This material has been prepared by Titanbay Ltd and its affiliates (together, “Titanbay”) and is provided for information purposes only. This document is directed at professional investors and qualified investors who have sufficient knowledge and experience to understand the risks of investing in private market investments.

This material should not be construed as legal, tax, investment advice or an invitation, general solicitation, recommendation, an opinion regarding the appropriateness or suitability of any investment strategy, or offer to buy, sell, or hold any investments or securities offered on or off the Titanbay investment platform. The views, opinions and estimates expressed herein constitute personal judgments of certain members of the Titanbay team based on current market conditions and are subject to change without notice. This information in no way constitutes Titanbay research and should not be treated as such. Any forecasts, figures, opinions or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions and are subject to change without prior notice.

All information presented herein is considered to be accurate at the time of production unless otherwise stated and has been prepared from sources Titanbay believes to be reliable. No representation or warranty or guarantee, express or implied, is given as to the truth, accuracy or completeness of the information or opinions contained herein and material aspects of descriptions contained in this material are subject to change without notice. No reliance may be placed for any purposes on the information or opinions contained in this material. Titanbay is not responsible for any error or omission in this material, nor do we accept liability for any losses arising from its use. Non-affiliated entities mentioned are for informational purposes only and should not be construed as an endorsement or sponsorship of Titanbay.

Investments in private placements and private equity investments via feeder funds in particular, are complex, highly illiquid and speculative in nature and involve a high degree of risk. The value of an investment may go down as well as up, and investors may not get back their money originally invested. Investors who cannot afford to lose their entire investment should not invest. Past performance, including simulated performance, is not a reliable indicator of future performance. For private equity investments via feeder funds, investors will typically receive illiquid and/or restricted membership interests that may be subject to holding period requirements and/or liquidity concerns. Investors who cannot hold an investment for the long term (at least 10 years) should not invest.

Titanbay Ltd is an Appointed Representative of Brooklands Fund Management Limited which is authorised and regulated by the Financial Conduct Authority with firm reference number 757575. Copyright Titanbay 2023.