Could rising interest rates trigger a stampede out of risky assets?

Warning: the following contains explicit language of a bearish nature. Readers of a more nervous disposition may want to look away now…

Even after three consecutive quarters of losses in both equities and bonds, investors may not be out of the woods. So far, it has been a painful, but orderly repricing of risky assets. Now, we fear something worse - a liquidation.

In a recent memo, Ruffer’s chief investment officer Henry Maxey suggests we could see a sudden rush for the exit by owners of risky assets such as equities and credit. Why might this happen?

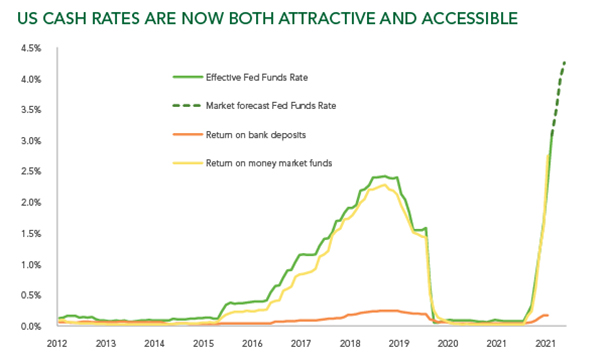

First and foremost, now there is an alternative. As the chart below shows, not only is the official US Federal Funds Rate now in excess of 3%, but ordinary US investors can access similar interest rates by investing in regulated money market funds (MMFs), which currently offer about 2.8%.

Never mind that banks in the US, just as in Britain, are still only offering derisory rates of interest on savings accounts. US investors now have access to safe savings vehicles offering interest rates of almost 3%.

Current market forecasts suggest that US interest rates will exceed 4% by the end of the year, a level MMFs look likely to match. History suggests that when interest rates move above 2%, investors start to take notice. A 4% return on cash may prove irresistible.

At the same time, savers pushed towards more risky investments in equities and credit, as an alternative to near zero interest rates, are probably now nursing hefty losses. How long before they decide they have had enough?

Sorry to pile on the gloom, but there are two further reasons why a switch out of equities and credit could be a disorderly rout, a liquidation event for financial markets, rather than the gradual withering of asset prices seen so far this year.

Regulators, mindful of the high risk of a global recession in 2023 and haunted by memories of the 2008 financial crisis, are discouraging commercial banks from expanding their balance sheets.

Meanwhile, the same banks face growing demands from companies in the real economy to fund inventories rising simply because of current inflation. These are profitable loans and look certain to receive priority over lending to financial institutions.

The search for yield drove many investors to seek extra income by tying up funds in illiquid investments such as private equity and private debt. If there is a rush to shift money into safer yet higher yielding assets, only a small pool of liquid assets can be sold quickly.

These are the reasons why we moved to a very cautious stance during the summer, with equity holdings as low as or lower than we held just before the global financial crash in 2008.

We would love to be more optimistic. But current events suggest now is not the time. As Ian Dury sang in 1979, it may be time for ‘A bit of grin and bear it’ before we can once again look for ‘Reasons to be cheerful’.

If you would like to a copy of Henry Maxey’s memo ‘So far, so good’, please email ruffer@ruffer.co.uk

Sources: Bloomberg, Ruffer

The views expressed in this article are not intended as an offer or solicitation for the purchase or sale of any investment or financial instrument, including interests in any of Ruffer’s funds. The information contained in the article is fact based and does not constitute investment research, investment advice or a personal recommendation, and should not be used as the basis for any investment decision. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. This article does not take account of any potential investor’s investment objectives, particular needs or financial situation. This article reflects Ruffer’s opinions at the date of publication only, the opinions are subject to change without notice and Ruffer shall bear no responsibility for the opinions offered. This financial promotion is issued by Ruffer LLP. Read the full disclaimer.