Easy money comes, easy money can go

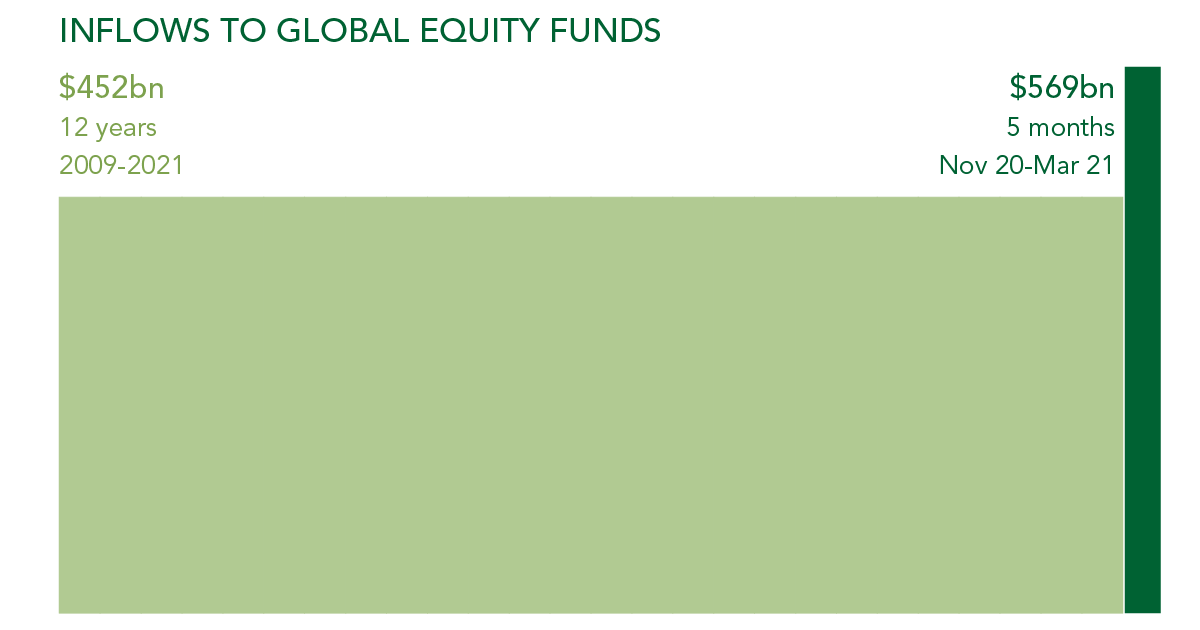

Over the past five months investors put more money into equity funds than in the previous twelve years combined. It’s easy to see why.

There is a lot of spare money around. Central banks have flooded the economy with support and generous government subsidies have filled the gap for millions of individuals. Those who could, saved.

Credit rating agency Moody’s estimate consumers around the world have increased their savings by $4.5 trillion since Covid-19 began, the equivalent of 6% of global gross domestic product.

One thing is clear—these savings are not going into conventional bonds, which have just suffered one of their worst quarters ever.

And why would they when the outlook for equities seems to be getting ever brighter? Consumer confidence has rebounded to pre-pandemic levels, activity is picking up and corporate earnings are rebounding strongly.

Source: Bank of America Global Investment Strategy, EPFR Global.

Investors are confronting the possibility that economic recovery—combined with continued monetary and fiscal stimulus—might also mark the end of the 40-year trend of falling interest rates and inflation, which has been so perfect for bonds.

At Ruffer we believe we are entering a new regime, which will be disastrous for conventional bonds. But what will this new regime—with the global economy poised for a growth spurt—mean for equities?

There is certainly scope for a considerable rebalancing out of bonds into equities. After all, since April 2009, $3 trillion of net inflows have gone into bond funds, much more than into equities, according to data from the Investment Company Institute.

But three things give us pause.

1. The best time to buy is when the news is bad. Now the news is improving, markets have been strong and valuations are generally expensive compared to history.

2. Markets have benefited from the almost ideal scenario of lots of money with nowhere to go. But as businesses gear up for re-opening and consumers have other ways of spending their money, liquidity will become less plentiful. And this is even before central banks and governments decide to press pause. A shrinking pool of liquidity could make things a lot bumpier.

3. Selectivity is going to be important. This is not a time for index funds. Investors have been fleeing bonds, but then buying bond-like equities. That means equities which benefit from the falling discount rates on long-term earnings—like technology and other long-term growth companies. The sort of strong recovery with pricing pressures we are expecting could be painful for these crowded positions.

So, we do think there is money to be made in equities. But following a period of such euphoria, we are taking some precautions. We’ve trimmed our overall exposure and we are tightly concentrated in equities and markets that are beneficiaries, not victims, of the conditions that will lead to higher interest rates.

So, we do think there is money to be made in equities. But following a period of such euphoria, we are taking some precautions. We’ve trimmed our overall exposure and we are tightly concentrated in equities and markets that are beneficiaries, not victims, of the conditions that will lead to higher interest rates.

And with bonds no longer likely to buffer the volatility in equities, investors will need to find an alternative. We have intensified the unconventional protections in our portfolio—designed to provide comfort during what could be a volatile ride.

Past performance is not a guide to future performance. The value of investments and the income derived therefrom can decrease as well as increase and you may not get back the full amount originally invested. Ruffer performance is shown after deduction of all fees and management charges, and on the basis of income being reinvested. The value of overseas investments will be influenced by the rate of exchange.

Past performance is not a guide to future performance. The value of investments and the income derived therefrom can decrease as well as increase and you may not get back the full amount originally invested. Ruffer performance is shown after deduction of all fees and management charges, and on the basis of income being reinvested. The value of overseas investments will be influenced by the rate of exchange.

The views expressed in this article are not intended as an offer or solicitation for the purchase or sale of any investment or financial instrument, including interests in any of Ruffer’s funds. The information contained in the article is fact based and does not constitute investment research, investment advice or a personal recommendation, and should not be used as the basis for any investment decision. This document does not take account of any potential investor’s investment objectives, particular needs or financial situation. This document reflects Ruffer’s opinions at the date of publication only, the opinions are subject to change without notice and Ruffer shall bear no responsibility for the opinions offered. Read the full disclaimer.