What can families learn from the succession woes of the Safra banking dynasty?

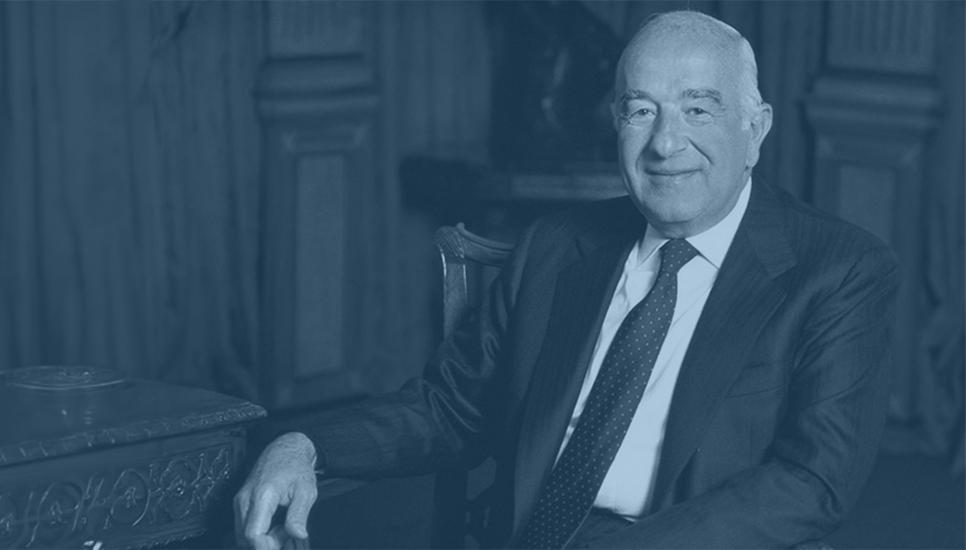

When Joseph Safra died in 2020 at the age of 82, little did he know that his passing would kickstart one of the bitterest succession battles in living memory.

Born and raised in Beirut, Lebanon, to a Jewish family that can trace its financial trading origins back to the height of the Ottoman Empire, Joseph had banking in his blood. In 1952, the Safras started a new life in Brazil which marked a new chapter in their storied history.

In 1956, Jacob Safra (founder of the Banque de Crédit National (BCN), one of the five oldest banks in Lebanon) and his eldest son Edmond, then 23, elected to make the seat of the family business Geneva, where they established the Trade Development Bank. Later, in 1966 and after Jacob’s death, Edmond further extended his financial reach with the establishment of the Republic National Bank of New York (which he sold to HSBC in 1999 and donated most of his money to the Edmond J. Safra Foundation).

Meanwhile, in 1955, Edmond’s younger brother Joseph opened a consumer credit company in Brazil that would eventually lead to the birth of Banco Safra, which grew under Joseph’s leadership to become the sixth largest bank in the country. His sibling Moise was a shareholder in the business and in 2006, Moise sold his remaining shares to Joseph.

Until the end of his life, Joseph retained control of the J. Safra Group, which now offers banking services in Europe, North America, and South America. It also acquired many residential and commercial real estate properties in the United States, Brazil and the United Kingdom – including the ‘Gherkin’ building in London and 660 Madison Avenue in New York.

According to Forbes, the assets over which Joseph had control were worth an estimated $22.8 billion, ranking him as the 52nd richest person in the world and richest in Brazil – an undeniably impressive legacy to leave behind. At the time of his death, Joseph already had donated the bulk of this wealth to his wife Vicky Safra (nee Sarfaty, the wealthiest Greek woman in the world), their three sons (Jacob, Alberto and David) and daughter (Esther, who is not directly involved in the family business).

However, the division that caused his sibling relationships to fracture throughout his own lifetime is now reflected in the dynamic between Joseph’s wife and three of their children on the one side and their middle son Alberto on the other, sadly devolving into a benchmark of how badly wrong a high-profile succession plan can go.

Alberto alleges in a lawsuit that, shortly after Joseph’s death, Alberto “learned he had been deprived of his rightful inheritance at the hands of his own mother and two brothers” – a claim the rest of the family strenuously insists is false. (Indeed, according to the family, Joseph gave Alberto $3.6 billion before he died.)

Regardless, the drama has continued to unfurl in the public domain as 43-year-old Alberto argues that he was wrongly disinherited following arguments with his younger brother, David, over control of Banco Safra. He claims that his father – who had been diagnosed with Parkinson’s disease – was medically unfit to sign the documents his family asserts were his final wishes.

The rest of the Safra family, meanwhile, claim that Joseph was “fully competent” and had complete “testamentary capacity,” as confirmed by multiple leading physicians and doctors, when Joseph reduced Alberto’s stake in the family business and altered his wills in late 2019. The real story, they say, is that a broken-hearted Joseph disowned Alberto for setting up a competitive banking venture, ASA Investments, and poaching the CEO and other senior employees of Banco Safra, despite his father’s entreaties and over his objections to his perceived disloyalty. The declaration was so definitive, it’s claimed by a family lawyer, that Joseph even barred Alberto from setting foot on the premises of his main Brazilian bank.

“The family regrets the path adopted by Alberto, who first attacked his father while he was alive and now does so against his memory, and refutes his allegations,” the family said in a statement in response to the lawsuit.

In his lawsuit, Alberto declares without providing any specific details that his mother and brothers had “engaged in acts of corporate misconduct to damage his interests in the company” – a claim the rest of the family denies.

“Due to illegal and aggressive acts committed by his brothers, Alberto Safra had no choice but to file a lawsuit with the Supreme Court of New York to protect his rights,” read a lawyers’ statement on behalf of Alberto. “The conduct alleged in this action was part of an ongoing, coordinated effort by the family defendants to dilute Alberto’s ownership interests in businesses owned by the Safra family around the globe, for which Alberto is seeking relief in multiple jurisdictions.”

The family has rejected this claim forcefully, including in a motion to dismiss a lawsuit Alberto filed in New York. "After Joseph’s death in 2020, the Plaintiff refused to accept the consequences of his own decision to leave the family business, and he launched a global campaign to dismantle his father’s last wishes by commencing legal proceedings around the world,” the motion reads.

The Safra story is very much a cautionary tale that should ring alarm bells with ultra-high-net-worth (UHNW) families around the world. Many UHNW families are experiencing a major succession shift (or that succession shift is on the horizon) and it has never been more important that every family member feels they have a voice.

As revealed in The 2023 North America Family Business Report from Brightstar Capital and Campden Wealth, 49% of UHNW respondents (49%) have experienced family conflict, which has often led to a breakdown in communication (according to 41% of respondents). The same report discovered that the majority of family businesses (61%) do not have a written, formal succession plan in place, while 44% still need to develop a succession plan or have no plan at all.

While the planning side of things doesn’t appear to be the Safras’ major issue, as (according to The Telegraph) “thanks to Joseph’s meticulous succession planning, eldest son Jacob was put in charge of operations outside Brazil, including J Safra Sarasin, a leading European private bank based in Basel”, while “the two younger brothers were made co-heads of Banco Safra. Alberto ran corporate banking and David, the youngest of the trio, was put in charge of individual and investment banking.”

The 2023 North America Family Business Report found that family conflict most likely arises from topics related to the roles and responsibilities of family members, succession planning, and the patriarch / matriarch unwilling to relinquish control (according to 41%, 27%, and 19% of respondents respectively). When asked about the outcome of their family conflict, four in ten respondents (41%) reported a breakdown of communication and continued family infighting. Meanwhile, 41% of respondents were able to avoid such adverse scenarios and resolve conflicts through regular family communication, followed by 31% who used the help of external advisors to settle disagreements.

“Breakdown in communication is what often leads to family conflict,” says Caroline Kitidis, Global Head of UHNW at HSBC Global Private Banking in an interview with CampdenFB. “These familial challenges are very personal. Many times, those involved try to manage within the four walls of their own home versus seeking advice from external counsel. Instituting forums and/or channels to do this can lead to establishing a healthy engagement model for the family members.”

Conflict can often arise as a result of mismanaged or misunderstood expectations.

In addition to creating ASA Investments after leaving the family’s bank in 2019, Alberto has subsequently launched several products, including a hedge fund and multi-market quantitative, equity and fixed-income strategies. He’s now reportedly looking to sell his share of the family’s banking interests as part of an ambitious plan to turn his own personal Family Office into one of the biggest in Latin America.

According to Bloomberg, the sale of his stake in the business could add $5 billion to his investment firm over the course of a decade. Under the terms of the proposed deal, however, Alberto would be barred from creating a new bank to compete with his brothers. Due to covering multiple jurisdictions, negotiations are expected to be ongoing for some time, but a deal would bring about the end of the ongoing wrangle.

Resolution may be in sight for what has been a very ugly and high-profile succession battle, but, says Russ Haworth, founder of The Family Business Partnership and host of The Family Business Podcast to CampdenFB, it could have all been avoided with clear communication. “Having conversations about how to deal with conflict doesn’t need to wait until conflict arises,” he says. “In fact, having these conversations prior to conflict being present is a good idea.

“Conflict can often arise as a result of mismanaged or misunderstood expectations. An exercise that I recommend families undertake to help mitigate this is what I refer to as ‘Lifeboat Drills’. These drills effectively simulate what would happen in any number of potential scenarios such as death, disability, divorce, disagreement etc, and ensures the family understands what currently happens to ownership, control and decision making in these scenarios, while also allowing them the time and opportunity to address any unintended consequences prior to the actual scenarios happening.

“Agreeing how you will deal with future disagreements or conflict may not necessarily help you to avoid them but knowing that you have a process in place that everyone feels is fair will provide reassurance that if it does happen, that there is at least a way to help you navigate it.”

Cognisant of the many governance issues families of wealth are forced to face, Campden Wealth has launched Campden Education, the first virtual training platform of its kind to empower families with practical knowledge and tools to make informed decisions. For further information, click here.