Taking back control' Demise of the deflation machine

In the late 1970s, the world was on the cusp of radical change. The ‘Deflation Machine’ was being born. Deng Xiaoping, having outmanoeuvred Mao Zedong’s preferred successor, began the process of reforming China’s moribund economy. In the West, liberal, free-market ideals were gaining traction, ideals that underpinned the subsequent regime of rapid, disinflationary global growth.

But this regime – propelled by economically desirable, yet politically intolerable, hyper-financialised supply chains – contained the seeds of its own demise. Its inherent contradictions were as much economic – higher inequality within economies was needed to reduce inequality between them – as they were political: a multilateral liberal world order required political power to be drained from national governments and their respective electorates.

A global financial crisis and pandemic-induced economic heart attack later, this regime is in its dying days. No one knows exactly what will follow, but the broad outline of the prospective paradigm is becoming clear. At its core will be ‘Strategic rivalry’ between the US and China, respectively the fading and rising hegemonic powers of the 21st Century [1]. Domestically, politics will become less internationalist, tolerant and laissez-faire and more nationalist, parochial and interventionist. ‘Who are we?’ and ‘What share of the pie will we get?’ are the questions that will dominate political discourse during the phase ahead of us, just as maximising growth of the national pie took centre stage in the one we are just leaving.

Our destination is a regime hostile to stable, non-inflationary growth. Globally, inflation is likely to be higher and more volatile. Inflation risk, an absent adversary throughout the careers of most investors today, will need to be priced once again. If a lack of inflation risk is the defining characteristic of today’s financial markets, its return will have profound consequences for prospective asset returns and cross-asset dynamics.

INFLATION RISK – THE ABSENT ADVERSARY

Where we are heading was the focus of my article in last year’s Ruffer Review. Its central premise was that the demise of the existing strong growth/low inflation regime started long before the pandemic. The events of the past two years are best viewed as accelerants of malign shifts in the global economy’s structural underpinnings. The pandemic matters not because it changes where we might end up (or why) but because it provides clarity on when we might arrive.

But left unsaid was what the journey might look like. Constructing a portfolio solely with the destination in mind without an eye on the potholes in the road is foolhardy. Somewhat counterintuitively, the journey is more uncertain than the destination. The core argument is, paradoxically, that the return of inflation risk might first lead us into a deflationary ditch – a painful outcome for any portfolio positioned solely for an inflationary future.

"A global financial crisis and pandemic-induced economic heart attack later, this regime is in its dying days."

The logic is as follows: Moderate inflation and depressed nominal risk-free interest rates are perceived as permanent features of the economic landscape and have become hardwired into investor behaviour [2]. Allocations to risky and illiquid assets have responded accordingly, driven higher by the combination of low volatility and non-existent returns on ‘Safe’ assets. This shift in portfolio structure has accelerated dramatically as nominal risk-free interest rates have fallen to zero [3].

If, or more likely when, central banks start to respond to persistent inflation by pushing short-term interest rates closer to historic norms, the reversal of these flows into illiquid corners of the market will occur in a non-linear and disruptive fashion. The withdrawal of policy stimulus is likely to include an end to large-scale asset purchases (and later active balance sheet shrinkage), the closure of emergency liquidity facilities and explicit guidance about a higher (conditional) path for policy interest rates.

This will expose the illusory and ephemeral nature of liquidity in the post-2008 financial ecosystem, what our CIO Henry Maxey has dubbed its ‘Avalanche prone nature’. If it is right that flows, rather than fundamentals, anchor asset prices in our financial system sanitised by quantitative easing (QE), the drawdown in risky assets could be dramatic.

A global financial crisis and pandemic-induced economic heart attack later, this regime is in its dying days.

THE FINANCIAL MARKET TAIL WAGS THE REAL ECONOMY DOG

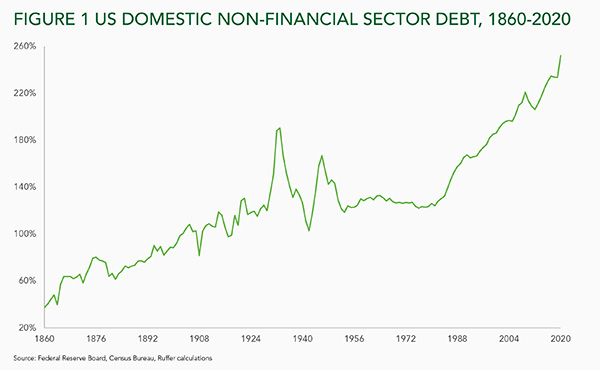

What the real economy needs today (higher interest rates) is something financial markets can’t stomach. But if the financial ecosystem has become so intolerant of policy ‘normalisation’, isn’t there a fundamental paradox, given the financialised and debt-laden nature of the economic system [Figure 1]?

The emergence of genuine inflationary dangers are anticipated to produce a policy response that, by triggering financial disruption, snuffs out the very thing that worried investors (and central bankers) in the first place. This would seem to confirm the belief that anchors today’s financial markets – the belief that the global economic system is inherently disinflationary [4].

This view is appealing and widely held, especially in the policymaking community. But it is likely to be wrong, for it ignores some crucial factors: politics and the social forces that shape the economic paradigm.

Financial conditions dance to the tune of central bankers. The more policymakers argue inflation will subside quickly and painlessly, the less likely it is to evolve that way. Why? Because perceptions of prospective inflationary dangers shape the message central bankers transmit into financial markets. If central bankers signal that they don’t believe much policy tightening will be needed, financial conditions will respond accordingly by barely tightening at all. The growth impulse from loose credit standards will remain considerable, and flows into illiquid corners of the financial ecosystem will remain substantial. At the core of this dynamic sits the reaction function.

This article was originally published in The Ruffer Review 2022. Download the full article here.

[1] Mearsheimer (2021), The Inevitable Rivalry: America, China and the Tragedy of Great Power Politics

[2] Cole (2017), Volatility and the alchemy of risk, Artemis Capital

[3] Lian & Ma (2018), Low interest rates and investor behaviour: a behavioural perspective, Federal Reserve Bank of Boston

[4] Borio & Disyatat (2014), Low interest rates and secular stagnation: is debt a missing link?, VoxEU

Past performance is not a guide to future performance. The value of investments and the income derived therefrom can decrease as well as increase and you may not get back the full amount originally invested. Ruffer performance is shown after deduction of all fees and management charges, and on the basis of income being reinvested. The value of overseas investments will be influenced by the rate of exchange.

The views expressed in this article are not intended as an offer or solicitation for the purchase or sale of any investment or financial instrument, including interests in any of Ruffer’s funds. The information contained in the article is fact based and does not constitute investment research, investment advice or a personal recommendation, and should not be used as the basis for any investment decision. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. This document does not take account of any potential investor’s investment objectives, particular needs or financial situation. This document reflects Ruffer’s opinions at the date of publication only, the opinions are subject to change without notice and Ruffer shall bear no responsibility for the opinions offered. Read the full disclaimer.