Jonathan Ruffer's Q3 investment review

When I was a boy, there was a programme on the telly where a smiley Arthur Askey interviewed ‘ordinary people’. It was more of a challenge than a conversation—if the interviewee replied “yes”, “no”, or “dunno”, there would be a sepulchral crash on a gong, wielded by a bruiser who specialised in frightening people. “What’s your name?” Askey would ask. “Ethel,” might be the reply. “Ethel?! That’s an old-fashioned name—what’s your middle name, then?” “Violet” the woman might say, a tremble in her voice. “Ethel Violet! I suppose you’ve got a brother called Claude!” “Oh no…” And bong would go the gong.

The pleasure was to watch people determined not to use the words, but out they’d pour anyway—and that’s what it feels like now in the investment world. The bears see nothing but scorched earth and Novichok. The bulls see nothing but free money freely dished out by governments and central banks. Each argument is a siren-voice persuading the already-persuaded of the strength of their belief.

Visit the Ruffer website

Visit the Ruffer websiteWhatever one’s outlook, there have been times in 2020 when the markets seemed to echo one’s innermost thoughts, and times when we shout out like Falstaff, that the whole world has gone mad. The bulls and the bears have had their time in the sun, and their time on the dark face of the moon—what follows is a digested diary of our journey through the year 2020 so far.

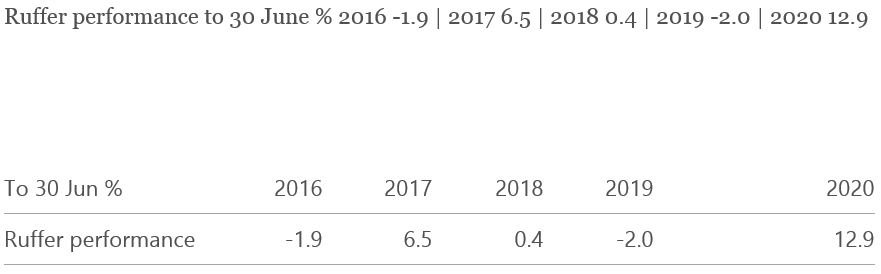

This year has been tricky for investors, because, out of the blue, two things became obvious – at the beginning of March, that one wanted to be in riskless assets; by the end of March, that one should be embracing risk. This sharp chicane was more than most people’s psyche could cope with. Sequentially, both types of investor were gonged out. As if to make a laughing stock of both extremes, at the time of writing this the US, German and Japanese stock markets are almost exactly unchanged, year to date. Now it happens that, over the same period, Ruffer’s performance is ahead of the pack—but the relevance of the performance is that our way of investment has kept our clients safe.

First, a declaration of bias. By nature, I am what Captain Barnaby’s nanny called ‘contradictorious’. This bull market is now in its 39th year—so the characteristic of being unconvinced by the prevailing wind is to be bearish. As I look round at colleagues, I see a mix of worriers and sun worshippers. But our investment style is neither. Our approach is about trying not to be wrong, rather than attempting to be right.

First, a declaration of bias. By nature, I am what Captain Barnaby’s nanny called ‘contradictorious’. This bull market is now in its 39th year—so the characteristic of being unconvinced by the prevailing wind is to be bearish. As I look round at colleagues, I see a mix of worriers and sun worshippers. But our investment style is neither. Our approach is about trying not to be wrong, rather than attempting to be right.

We entered 2020 with one settled thought: that the longstanding impasse—no growth, and abnormally low interest rates—would, sooner or later, be broken by the re-emergence of inflation. We therefore held assets which would benefit from this phenomenon. Inflation-linked bonds are the locus classicus—and we came into the year with plenty of them. Gold is a shadowy investment—many refuse even to recognise it as such, regarding it as a speculation—but it did superbly in the inflationary 1970s, and if people get afraid of paper and intangible assets, there’s nothing as good as gold (excepting a gold digger—so we favoured gold mining shares over gold bullion). These big positions were a risk, if we were wrong. Even if we were only wrong for a while, we’d have too much of the portfolio taking a hit. So we held investments which benefitted from the opposite of the phenomenon we expected—namely, rising interest rates. We had investments that would profit handsomely from a sell-off in risky corporate bonds, and we embraced equities in the banking sector. At the same time, global growth was looking as if it would be improving—and the UK, mired in Brexit-blues, looked to benefit from a combination of the unexpectedness of UK strength, and the growth itself. A comparatively small weighting of cyclically-based shares in UK plc could, we felt, act as an effective counterweight within portfolios.

Covid-19 made monkeys out of this last idea. Britain proved once again to be a nation of shopkeepers and service industries, centred on the metropolis—and the banks were almost the worst place to be. As the virus changed the behaviour of societies in a way comparable to a declaration of war, the markets were totally unprepared. The falls in March were quick and severe. In Ruffer portfolios, we had small amounts of powerful protection for a market break—precaution based not on a thimbleful of insight about a pending pandemic, but on buckets of concern about the imbalances in a structural bull market. As the helter spiralled into skelter, our catastrophe insurance—based on a volatility index called the VIX—performed handsomely, doing all we hoped it would. Our positions to profit from stress in corporate credit markets, increased in the previous three months, also served portfolios well, as did our put options on the US and European equity markets. In the heat of the battle, distressed selling began to threaten our core positions, just as happened in 2008: anticipating gold’s vulnerability, we bought protective options on gold bullion.

Covid-19 made monkeys out of this last idea. Britain proved once again to be a nation of shopkeepers and service industries, centred on the metropolis—and the banks were almost the worst place to be. As the virus changed the behaviour of societies in a way comparable to a declaration of war, the markets were totally unprepared. The falls in March were quick and severe. In Ruffer portfolios, we had small amounts of powerful protection for a market break—precaution based not on a thimbleful of insight about a pending pandemic, but on buckets of concern about the imbalances in a structural bull market. As the helter spiralled into skelter, our catastrophe insurance—based on a volatility index called the VIX—performed handsomely, doing all we hoped it would. Our positions to profit from stress in corporate credit markets, increased in the previous three months, also served portfolios well, as did our put options on the US and European equity markets. In the heat of the battle, distressed selling began to threaten our core positions, just as happened in 2008: anticipating gold’s vulnerability, we bought protective options on gold bullion.

Over the period of the lows, we liquidated all of our protective options, increasing the risk of portfolios materially. This might seem an obvious thing to do with hindsight, but it certainly didn’t feel obvious at the time. At the worst moment in March, the US equity market had dropped by 34% from its high, and could have plunged further. At their worst point, Ruffer portfolios were down around 2% for the year.

We took it for granted that the central banks would respond with immoderate athleticism to the cratering of the market. When gold and inflation-linked bonds fell sharply, we returned to large weightings in both these assets, tarnishing the excellence of the timing by selling down some equities, particularly oil stocks, right at the bottom. We therefore caught the sharp recovery in the markets, but largely missed the surge in technology stocks—despite the pleas of some of Ruffer’s best analysts, who were urging us to invest in what, as it turns out, have been some of the very best names. Why didn’t we buy them? Not because we faulted the analytical work. Rather it was because technology stocks are yet more long-duration assets—meaning it is their long-term earnings power (discounted at lower and lower interest rates) which became, in the eyes of the market, more and more valuable. We felt we had more than enough of those characteristics elsewhere in the portfolio—and in less crowded opportunities. What we struggled to have were enough cheap cyclical stocks—cheaply rated, and where all the value is in earnings that will be delivered in the next three or so years. We could see the portfolios were fine for Armageddon—but suppose there was… a vaccine? We would have been exposed to many of the wrong things as the economy roared back to life—in a scenario where central banks, with a sigh of relief, could get interests up a bit to give the hard-pressed saver a sprinkling of income.

We took it for granted that the central banks would respond with immoderate athleticism to the cratering of the market. When gold and inflation-linked bonds fell sharply, we returned to large weightings in both these assets, tarnishing the excellence of the timing by selling down some equities, particularly oil stocks, right at the bottom. We therefore caught the sharp recovery in the markets, but largely missed the surge in technology stocks—despite the pleas of some of Ruffer’s best analysts, who were urging us to invest in what, as it turns out, have been some of the very best names. Why didn’t we buy them? Not because we faulted the analytical work. Rather it was because technology stocks are yet more long-duration assets—meaning it is their long-term earnings power (discounted at lower and lower interest rates) which became, in the eyes of the market, more and more valuable. We felt we had more than enough of those characteristics elsewhere in the portfolio—and in less crowded opportunities. What we struggled to have were enough cheap cyclical stocks—cheaply rated, and where all the value is in earnings that will be delivered in the next three or so years. We could see the portfolios were fine for Armageddon—but suppose there was… a vaccine? We would have been exposed to many of the wrong things as the economy roared back to life—in a scenario where central banks, with a sigh of relief, could get interests up a bit to give the hard-pressed saver a sprinkling of income.

Where are we now? In portfolios, we have to guard against a vaccine and a marked improvement in the economic outlook. And we have to guard against a slump so deep that any talk of inflation is seen as a phantom of the passing night. Like every other investor in the world, we yearn to have safe income—and like the rest of the world, we cannot see it. It is here we part company with the consensus. As the income seeker chases more and more uncertain opportunities, we hold positions to benefit from signs of vulnerability in the junk bond market, a market that has been distorted by yield-chasing flows and (since March) the backstop of the US Federal Reserve. We are intrigued by Japan, which has been living in the zombie world of no interest rates for a generation; in the recovery it led to good equity investments, and now we have an amplified currency position in the Japanese yen. This yen position was bought cheaply, and in size—it has the power to be a real protection for the manifold risks we face if we enter a world where our cyclical stocks prove inappropriate. Perhaps, now that it isn’t priced, the UK might find a Brexit deal and a vaccine. But so far our UK banking stocks—which have fallen by more than almost everything – have resolutely failed to bounce. That is the price we (you) have paid for other things in the portfolio which have worked.

Where are we now? In portfolios, we have to guard against a vaccine and a marked improvement in the economic outlook. And we have to guard against a slump so deep that any talk of inflation is seen as a phantom of the passing night. Like every other investor in the world, we yearn to have safe income—and like the rest of the world, we cannot see it. It is here we part company with the consensus. As the income seeker chases more and more uncertain opportunities, we hold positions to benefit from signs of vulnerability in the junk bond market, a market that has been distorted by yield-chasing flows and (since March) the backstop of the US Federal Reserve. We are intrigued by Japan, which has been living in the zombie world of no interest rates for a generation; in the recovery it led to good equity investments, and now we have an amplified currency position in the Japanese yen. This yen position was bought cheaply, and in size—it has the power to be a real protection for the manifold risks we face if we enter a world where our cyclical stocks prove inappropriate. Perhaps, now that it isn’t priced, the UK might find a Brexit deal and a vaccine. But so far our UK banking stocks—which have fallen by more than almost everything – have resolutely failed to bounce. That is the price we (you) have paid for other things in the portfolio which have worked.

As I read through this review, I find myself thinking—Volvo, handbook, about as exciting as. But even a Volvo manual is of interest in the right circumstances. And all investors have a right to know not only the constituent parts of the portfolio but also the minds behind the hands that make the allocations.

In summation, this year we have taken the difficult road to safety, the road of active trading—not trading to speculate on perceived opportunities, but trading to ensure the portfolio is constantly in balance. It is worth considering what the easy route to a successful portfolio in 2020 would have been. Looking back, the easiest of them all would be a big overweight in Amazon and pals—fast-growing and undertaxed businesses which dominate their sectors, and where Covid-19 has blown a mighty following wind. The other route was to spot that pressure on central banks to cut interest rates further would be irresistible—so buy government bonds quickly, before the central banks beat you to it. Those who have done either or both of these things have had another good year—but a change in a single variable will sideswipe both those asset classes at the same time. Their dynamics feel very different, but actually, they are not. I wouldn’t argue against momentum-driven stocks on fundamentals (although a trillion dollars for one company seems like a lot of money; I could definitely see Las Meninas by Velazquez fetching that… but a mere corporation?). The issue is in the world of fear and greed, fear has jumped over to the other side, and people fear not holding these stocks. It does not need disillusionment, or poor fundamentals—simply an understanding that you don’t have to own any particular asset class, even this one. Such realisation happens as a revelation: “the scales fell from my eyes” (although I doubt St Paul was thinking of Tesla when he said it).

In summation, this year we have taken the difficult road to safety, the road of active trading—not trading to speculate on perceived opportunities, but trading to ensure the portfolio is constantly in balance. It is worth considering what the easy route to a successful portfolio in 2020 would have been. Looking back, the easiest of them all would be a big overweight in Amazon and pals—fast-growing and undertaxed businesses which dominate their sectors, and where Covid-19 has blown a mighty following wind. The other route was to spot that pressure on central banks to cut interest rates further would be irresistible—so buy government bonds quickly, before the central banks beat you to it. Those who have done either or both of these things have had another good year—but a change in a single variable will sideswipe both those asset classes at the same time. Their dynamics feel very different, but actually, they are not. I wouldn’t argue against momentum-driven stocks on fundamentals (although a trillion dollars for one company seems like a lot of money; I could definitely see Las Meninas by Velazquez fetching that… but a mere corporation?). The issue is in the world of fear and greed, fear has jumped over to the other side, and people fear not holding these stocks. It does not need disillusionment, or poor fundamentals—simply an understanding that you don’t have to own any particular asset class, even this one. Such realisation happens as a revelation: “the scales fell from my eyes” (although I doubt St Paul was thinking of Tesla when he said it).

The other asset class, the fixed interest market—in top government stock—is not about fear and greed: it is about understanding the chess game which plays out between the authorities and the investment community. The authorities hate being in low-yield (pushing into no-yield) territory, but the markets won’t let them out. Yet bull-baiting can backfire—when circumstances change, then so, quickly, can the nature of the game. Today government bonds are held for the locked horns with the authorities, and high-yields are held for the brackish moisture which passes for yield in this strange world. If inflation comes about—or, rather, looks like a realistic possibility—you won’t see government bonds or tech stocks for dust.

The other asset class, the fixed interest market—in top government stock—is not about fear and greed: it is about understanding the chess game which plays out between the authorities and the investment community. The authorities hate being in low-yield (pushing into no-yield) territory, but the markets won’t let them out. Yet bull-baiting can backfire—when circumstances change, then so, quickly, can the nature of the game. Today government bonds are held for the locked horns with the authorities, and high-yields are held for the brackish moisture which passes for yield in this strange world. If inflation comes about—or, rather, looks like a realistic possibility—you won’t see government bonds or tech stocks for dust.

For our part, we will periodically fail to make decent money—including a three year dry run to spring 2019—as we seek to make time a friend, and allow money-value to accumulate. There’s always the possibility that Ruffer will snatch defeat from the jaws of victory, finding an eccentric way of losing a packet. But—and here’s the boast—we never have, in 27 years, mislaid that packet. We sometimes liken investment to the art of juggling grenades—Ruffer puts a premium on keeping the pins in place.

Past performance is not a guide to future performance. The value of investments and the income derived therefrom can decrease as well as increase and you may not get back the full amount originally invested. Ruffer performance is shown after deduction of all fees and management charges, and on the basis of income being reinvested. The value of the shares and the income from them can go down as well as up and you may not get back the full amount originally invested. The value of overseas investments will be influenced by the rate of exchange. Ruffer LLP is authorised and regulated by the Financial Conduct Authority. © Ruffer LLP 2020. Registered in England with Partnership No OC305288. 80 Victoria Street, London SW1E 5JL ruffer.co.uk

Past performance is not a guide to future performance. The value of investments and the income derived therefrom can decrease as well as increase and you may not get back the full amount originally invested. Ruffer performance is shown after deduction of all fees and management charges, and on the basis of income being reinvested. The value of the shares and the income from them can go down as well as up and you may not get back the full amount originally invested. The value of overseas investments will be influenced by the rate of exchange. Ruffer LLP is authorised and regulated by the Financial Conduct Authority. © Ruffer LLP 2020. Registered in England with Partnership No OC305288. 80 Victoria Street, London SW1E 5JL ruffer.co.uk