Environment, social and governance risks are financial risks

Russell Investments has a long history of highlighting the role of environment, social and governance (ESG) factors in adding value to an investment practice (1). In this post, we share three proof points of the value-add associated with ESG awareness and integration, and analyse the importance of considering ESG risks both in the security selection process and the asset manager selection process.

Ultimately, we believe that investors who are unaware of ESG and do not integrate ESG into their investment processes may be exposing themselves to additional, unnecessary and possibly unrewarded risks.

Proof point #1: Selecting securities without considering ESG may be risky business

On 20 April, 2010, the Deepwater Horizon oil drilling rig, located in the Gulf of Mexico, exploded—killing 11 workers and creating the largest oil spill (pictured_ from a drilling rig in history. Eventually, 4 million barrels of oil poured into the Gulf of Mexico, creating extensive damage to air, water and recreational quality along coastal states. Marine life, fisheries, land and air wildlife, businesses and port users were all severely impacted. Ultimately, the damage just to natural resources was estimated at $8.8 billion (2). BP (formerly known as British Petroleum) lost 51% of its market value in 40 days following the explosion, and ultimately paid $28 billion (3) in response and clean-up efforts.

What made headlines about the Deepwater Horizon spill was the environmental impact. We heard less about what was truly behind that environmental disaster—the below-peers safety practices (4) that fostered the explosion (a social characteristic) and the lapses in oversight (5) and accountability (a prominent governance issue). This leads to the fundamental question—should we have known?

What made headlines about the Deepwater Horizon spill was the environmental impact. We heard less about what was truly behind that environmental disaster—the below-peers safety practices (4) that fostered the explosion (a social characteristic) and the lapses in oversight (5) and accountability (a prominent governance issue). This leads to the fundamental question—should we have known?

BP’s governance issues were well-known and easy to discover by quality security analysis. As the Harvard Business Review put it in 2010: “BP must also clean up an organisational and cultural mess… Lapses seem to have been everywhere; e.g., in preparedness, alert systems, communication, and worst ¬case [sic] scenario plans” (6).

Likewise, BP’s safety issues were also well-known and easy to discover by quality security analysis. With multiple fines for violating laws regarding hazardous waste going back to 1990, the company had “one of the worst worker safety records among large industrial companies operating in the United States” (7). The combination of lapses and poor worker safety should have been red flags for anyone reviewing these securities.

Considering ESG is consistent with good securities analysis that has always been part of a review and selection process.

Proof point #2: Asset managers may improve outcomes by considering ESG risks and opportunities

We evaluated the return differential from asset managers who integrated ESG well into their investment practice relative to those who did not. In addition, we evaluated the return differential from equity products with lower ESG-related risks to those with higher ESG-related risks. In both cases, we found evidence that considering ESG produced a return premium.

Proof point #2.1 Qualitative ESG rankings for equity and fixed income

Russell Investment has, since 2014, ranked active managers on their ESG consideration and implementation, based on qualitative assessments of their processes, product by product (8) In examining excess returns by ESG rank groupings, we found a modest return to higher ESG-ranked equity and fixed income products, shown in Table 1 below.

Table 1. ESG returns by group over 1-, 3-, and 5-years from December 2019

Bold figures: Indicates 95% confidence level.

Italics: Indicates 90% confidence level.

In reviewing the left half of the table, we noted that length of the historical period matters in evaluating equity returns (9):

• Jan 2015-Dec 2019 (5 years, annualised): Higher ESG rank products exhibited a statistically significant return premium

• All shorter historical periods: Higher ESG ranked products exhibited a statistically insignificant return premium

In reviewing the right half of the table, we observed almost exactly the opposite time effect for fixed income products.

• Jan 2019-Dec 2019 (1 year, annualised) and Jan 2017-Dec 2019 (3 years, annualised): Higher ESG rank products exhibited a statistically significant return premium.

• Jan 2015-Dec 2019 (5 years, annualised) and Jan 2020-Mar 2020 (1 quarter, unannualised) Higher ESG rank products exhibited a statistically insignificant return discount.

Ultimately, it appears that the long-term favours ESG for equity products, but only some periods favour ESG for fixed income products. Moreover, the first quarter of 2020—punctuated by the broad Covid-19 market event—had an impact on both equity and fixed income markets, but the cross-sectional volatility of active returns precluded any statistically significant differences based on ESG rankings.

Quantitative ESG risk ratings (equity products only)

Russell Investments measures ESG risks in all equity products using an external data provider (Sustainalytics), with lower numbers indicating lower ESG-related risks.10

Because Sustainalytics changed its methodology in 2019, we have a very short history of live data and cannot make strong assertions. We can, however, evaluate Q4 of 2019 and Q1 of 2020 excess returns using the live Sustainalytics ESG risk ratings from start-of-quarter risk ratings. We tested the differences in excess returns for several universes and over 1,800 equity products (11). To provide a historical perspective reflecting the evolving nature of risk ratings data, we used some back-test data for two universes U.S. large cap and global equities (12)—to demonstrate year-by-year differences in excess returns.

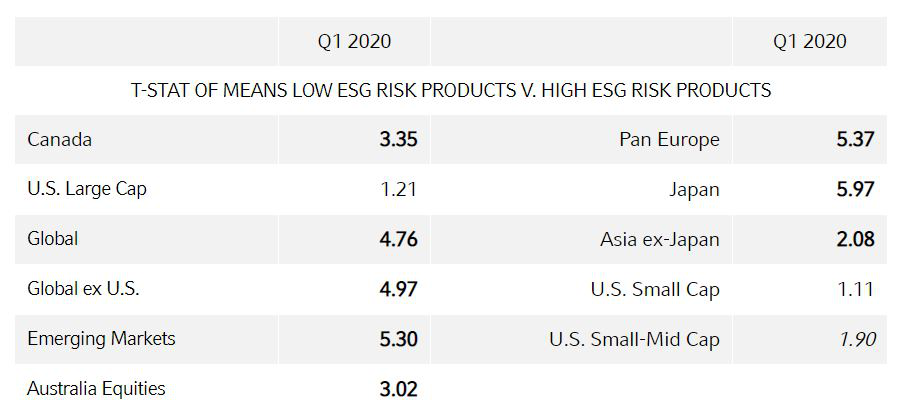

In Table 2, we compared the excess returns of portfolios in the two lower ESG-related risk quintiles to the excess returns of portfolios in the higher three ESG-related risk quintiles.

Table 2. Means tests of excess returns, low v. high ESG-related risks 2015 - 2020 Q1

Bold figures: Indicates 95% confidence level.

Italics: Indicates 90% confidence level.

Notably, in four out of five years, portfolios with low ESG-related risks (as measured by this particular metric) produced significantly higher excess returns for U.S. large cap and global equity portfolios. The material exception is 2016. In 2016, low ESG-related risk portfolios produced significantly lower excess returns for these same equity universes.

For Q1 2020, we had live data to exhibit and details on more securities. We show these details in Table 3. In evaluating these two quarters, we observed that lower ESG-related risk was universally rewarded across these universes—with a statistically significant premium in eight of 11 universes. This relationship was upheld despite the Covid-19 market selloff.

Table 3. Means tests of excess returns, low v. high ESG-related risks 2020 Q1

Bold figures: Indicates 95% confidence level.

Italics: Indicates 90% confidence level.

Excess returns and standard deviations are not annualised.

From this data analysis, we conclude that considering ESG in the investment process may have improved returns for both equities and fixed income portfolios in recent years.

Proof point #3: ESG consideration is a standard feature of current investment practice

Our 2020 ESG manager survey demonstrated that the vast majority of managed assets incorporate quantitative and qualitative information into their ESG assessments (13).

To further assess when ESG factors play a role in investment decisions, we asked managers when should ESG factors dominate investment decisions (outside of investment guideline considerations). Results show that the financial materiality of ESG factors is a focal point for the decision-making process. Some 63% of the survey respondents claim to incorporate specific ESG considerations when the materiality is high, versus 55% from the previous year.

The bottom line: ESG is value-adding to a skilled investment practice

Ultimately, there is a growing consensus among the investment management industry that integrating ESG factors into an investment practice is value-adding. Understanding ESG characteristics may certainly shed light on risks that need to be managed or considered, and we believe that returns will ultimately reflect this reality.

Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.

1 Some recent examples are Negative screening and performance, The unintentional biases of ESG portfolios, Doing well by doing good.

2 https://www.epa.gov/enforcement/deepwater-horizon-bp-gulf-mexico-oil-spill

3 https://hbr.org/2010/06/bps-tony-hayward-and-the-failu.html

4 https://www.corp-research.org/BP

6 https://hbr.org/2010/06/bps-tony-hayward-and-the-failu.html

7 https://www.corp-research.org/BP

8 As of the writing of this note, Russell Investments has ranked nearly 100% of our high interest managers across equities, fixed income and alternatives. Note that it is more likely that ESG ranks have been assigned to high interest products - these products include Hire (or 4) and Retain (or 3). We have also ESG-ranked many of our Watch (or 2) and Fire (or 1) ranked products, and a handful of unranked products (mostly the A or B). The bias lies in that we have more ESG-rank information on those products we are likely to use and recommend than otherwise.

9 Note that we do not control for skill in any way, but rather look across the active universes and compare each product with its own benchmark.

10 We also measure these risks for all Russell Investments’ equity and fixed income funds. Risk ratings require holdings to assess and we are more likely to have holdings for products we are more likely to use and recommend.

11 Note that the live risk ratings data is slightly different, with more underlying information, than the historical back-tested data exhibited in Table 5.

12 Approximately 400-650 active products.

13 See 2020 Annual ESG Manager Survey by Yoshie Phillips.

Important information

Important information

Unless otherwise specified, Russell Investments is the source of all data. All information contained in this material is current at the time of issue and, to the best of our knowledge, accurate. Any opinion expressed is that of Russell Investments, is not a statement of fact, is subject to change and does not constitute investment advice.

Issued by Russell Investments Limited. Company No. 02086230. Registered in England and Wales with registered office at: Rex House, 10 Regent Street, London SW1Y 4PE. Telephone +44 (0)20 7024 6000. Authorised and regulated by the Financial Conduct Authority, 12 Endeavour Square, London, E20 1JN. Russell Investments Limited is a Dubai International Financial Centre company which is regulated by the Dubai Financial Services Authority at: Office 4, Level 1, Gate Village Building 3, DIFC, PO Box 506591, Dubai UAE. Telephone + 971 4 578 7097. This material should only be marketed towards Professional Clients as defined by the DFSA. Russell Investments Ireland Limited. Company No. 213659. Registered in Ireland with registered office at: 78 Sir John Rogerson’s Quay, Dublin 2, Ireland. Authorised and regulated by the Central Bank of Ireland.

KvK number 67296386

©1995-2021 Russell Investments Group, LLC. All rights reserved.

MCR-00955