Betting on a troubled world

In terms of performance, hedge funds have had it rough the past few years. And of all the alternative investment styles, global macro has arguably had it the worst. Global macro strategies try to forecast macroeconomic developments around the world, such as interest rates, geopolitics, government policies and so on.

US investment wizard George Soros famously employed the strategy in the early 1990s, betting against the British pound, which earned him the moniker “the man who broke the Bank of England”. The move earned him more than $1 billion (€785 million).

This, of course, is a rare scenario, and indices from the past three years show macro funds have been poor performers. In 2011 the Barclay Global Macro Index was down 3.65% year-on-year. The style struggled through 2012, attaining less than 2.6%, and making only 4.81% last year. As of August this year, the Barclay Global Macro Index has been negative as many months as it has positive, and is on track to sink back below the 3% mark for the entire year.

With such pitiful returns, is it any wonder why global macro investing has fallen out of favour with many family offices?

Indifference to the style should not translate into ignorance of the geopolitical climate and macroeconomic data, warns Steven Drobny, founder of Santa Monica-based Drobny Capital and author of Inside the House of Money.

What geopolitical factors then should families take into account when investing? Is scenario planning useful? What processes can they employ to mitigate risk? And does your family have its own personal foreign policy?

“Global macro is the hardest strategy to understand in the hedge fund space because of its breadth of instruments, markets, and inherent complexity, but the macro world is the driver of everything,” says Drobny. “You can't just pick a stock based on fundamentals without understanding how it can be impacted by geopolitical risk, the price of oil, interest rates and other macroeconomic issues.”

For most developed-world family offices, Drobny says if you're looking to diversify your portfolio, there are not a lot of opportunities within the highly correlated world of fixed income and equities. You need to look at global macro exposure.

“You don't need to be a 'macro guy' trading fixed income arbitrage opportunities or frontier market sovereign bonds – or even put all your money in macro hedge funds. But you do need global macro exposure, as well as an understanding of what implicit macro bets you have in your broader portfolio,” says Drobny. “You need to look forward, not backwards, which means maintaining a strong understanding of how the world may evolve.”

Drobny does not think family offices should have all their assets tied up in hedge funds: “But you should have some exposure. Use hedge funds to gain exposure that you can't get yourself, or to help you do a better job as an asset allocator – especially if you are headcount constrained and don't have the time to do deep analysis yourself.”

Drobny argues that from an analytical perspective, macro as a strategy provides more access to information than other hedge fund strategies. He suggests using hedge fund exposures not only as strategic growth assets, but also as a way of accessing the intellectual property and actionable information that hedge funds have: “Utilise your hedge fund programme to expand research capabilities and supplement internal expertise, so that you can: better understand the macro environment; provide expertise for structuring and implementing investment themes across asset classes; and assist in the risk management process for tactical decisions, stress testing, tail hedging and asymmetric investment opportunities.”

Winter is coming

Andre Stein has been closely observing and analysing global political and military activity and its effects on capital markets for more than a decade. He predicts that the northern winter of 2014/15 could be a harsh geopolitical season. Three years ago, Stein, a former adviser to governments on the impact of national security on economic management, began advising family offices with global macro portfolios, on the impacts of geopolitical events. The central figure to watch in the next few months, says Stein, is Russian president Vladimir Putin. He is likely to up the ante even further in his conflict with the West and assert even more influence on the international stage.

Putin has a history of capitalising when the world's attention is diverted by elections, holidays and other events, says Stein. “During the past decade he has often timed activities, such as disrupting cross-border energy supplies, around the holidays when policymakers are on vacation or otherwise occupied. And November through to January 2015 will prove to be extremely busy.”

Putin has a history of capitalising when the world's attention is diverted by elections, holidays and other events, says Stein. “During the past decade he has often timed activities, such as disrupting cross-border energy supplies, around the holidays when policymakers are on vacation or otherwise occupied. And November through to January 2015 will prove to be extremely busy.”

November sees the US midterm elections, which will decide whether the Democrats can keep the Senate and the Republicans win more ground in the House of Representatives. In the US, Ebola, Syria and Iraq continue to dominate the headlines, but the real domestic risks may just be over the horizon.

“Don't forget,” says Stein, “the US debt ceiling issue has not been resolved permanently. Both Republicans and Democrats decided on a temporary fix until shortly before the midterms. After January 2015 there is a real risk the debt ceiling will come back with a vengeance, creating more domestic uncertainty. President Putin is a supreme political opportunist and if the White House and Congress are distracted by a major debt ceiling showdown, this provides additional incentive for Putin to act – particularly as he is under pressure from low oil prices.”

Closer to Russia, Moldova and Romania have their own elections in November. “While these two countries by themselves are not of particular importance to the average family office, Russia has reputedly poured significant amounts of resources and effort into these elections, relative to their size,” says Stein. “If Putin doesn't get a favourable outcome, this may exacerbate his need to make up for lost ground elsewhere.”

Much of Eastern Europe is heavily reliant on Russian gas. A “temporary” supply disruption or other warning signals would add to the sense that EU Member States and aspirant country candidates are vulnerable to Kremlin decision-making.

Over the past few months, Russia has been challenging air defence zones around its opponents' borders. In late October, a Russian spy plane flew into Estonian airspace – the most serious violation of Nato airspace since the end of the Cold War: “Lately, Putin has been pushing fighters and strategic bombers into European airspace, with no effective retaliation from the EU member states or the US. From where Putin sits in the Kremlin, Nato's doctrine of collective defence looks increasingly fragile.”

Stein highlights what he considers to be three key factors that make the current situation so dangerous: (1) Not since the Cold War has Russia been so aggressive, (2) European militaries have never been so weak, and (3) The will to confront Russia – including using military deterrence – has never been so low.

Most of all, says Stein, a further bad set of German production numbers, combined with the expected decline of Chinese economic indicators would create a double blow to global economic sentiment, increasing investor nervousness.

For investors, Stein thinks this all points to a number of possibilities: “Parts of the financial markets could experience significant volatility, exacerbated by thinner trading volumes. During times of geopolitical upheaval, markets often see a flight to safety assets, such as the US dollar, treasuries or even gold, while the euro and key emerging markets currencies experience sharp falls. Capital outflows from emerging markets could increase even further when these factors are combined with sentiment surrounding the winding down of quantitative easing.”

From these events, there are myriad investment implications. Stein says families would do well to review their portfolio to identify areas of risk so that they can hedge. Families should keep a close eye on volatility indexes (such as the VIX, which tracks the S&P 500 and the VSTOXX Indices, based on the EURO STOXX 50), with a view to utilising them for hedging purposes. However, Stein warns: “These indices are also traded for their technicals, so they're not always absolute indicators of risk. But they are useful tools – especially if trading volumes are thin.”

On the other hand, for the adventurous family office with significant risk appetite, there are always bargains to be had in any market sell-off. Brent futures, movements in the Russian credit markets, and statements from the Russian and emerging market central banks could also be important indicators over the coming quarters, says Stein.

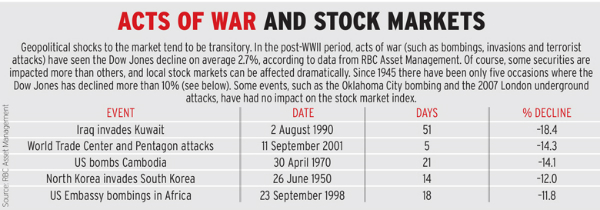

“Increases in global risk don't always have a direct impact on the markets,” says Stein, pointing out that many of the countries in conflict areas have relatively small GDPs. Research from RBC Asset Management estimates that market corrections due to acts of war have averaged less than 3% since 1945 (see box-out).

“Sometimes the market impact is sector specific, like travel, banking or energy. But it is always important to understand the potential impacts on your portfolio and do some basic scenario planning.”

Big picture or fine detail?

Attaining an understanding of geopolitics is critical to managing an international portfolio, asserts the principal of an Oklahoma-based family that made its fortune in oil, and still has substantial holdings both domestically and abroad.

“Sometimes it's simply a matter of keeping abreast of the news and taking the time to ponder 'what if' on any given situation,” says the principal, on the condition of anonymity so that he could speak freely about his investment decision-making. “But often times we do extensive scenario planning to understand how certain events could impact our holdings.”

Only recently, the family has looked closely at the outbreak of Ebola in Western Africa. “We have many holdings in Africa and we wanted to make sure we understood the implications of the outbreak.”

Issues they considered were widespread infection in markets in which they operated, the effects on transport systems and healthcare, and the impact on oil prices.

Scenario planning – once the exclusive domain of governments' security and defence communities – has become an increasingly important strategic planning tool for investors. Stein, who has advised several governments on issues impacting security and economic decision-making and foresight, often helps families model scenarios which could impact their investments.

“Scenario planning allows you to establish an understanding of possible alternative futures and determine the impact of these futures on your investment strategy. [You can] gain some foresight and guidance on how to successfully deal with these impacts,” says Stein.

Yet for some investors, global macro data is less valuable than approaching investments from a micro perspective. “I don't see the need to look too closely at global macro data,” says Heinz Blennemann, principal at Californian single family office Blennemann Family Investments. As a long-term investor, he uses a barbell approach with mainly private debt and equity/private equity.

“Private debt performs whether the market is going up, down or sideways and is uncorrelated to the global scene. My private equity holdings are keenly based on the individual opportunities. They have very long event horizons,” he says.

While he has investments in Asia, Africa, Latin America, and other emerging markets, Blennemann says he is not looking at these markets necessarily because of their macro or geopolitical environment. “I'm trying to find inefficiencies in the markets and invest in pockets where there are niche, underserviced opportunities. I'm looking for really good managers at the company level, with great track records. And that's something that macro data won't give you.”

To Blennemann's mind, global macro hedge funds are in the business of predicting where markets are going to be in around three-to-five years, or where there will be extraordinary flare-ups.

“This is really difficult to do consistently. Many of the geopolitical and macroeconomic episodes that happen in the world are hard to predict; even the legions of PhDs at [the US Federal Reserve] did not predict the severity of the real estate bubble. They may seem obvious after the fact, but that doesn't mean they could've been predicted. Global macro is often added to a portfolio to add diversification in strategy. However, global macro returns historically have been very volatile. The way I prefer to mitigate my equity/private equity exposure is by adding private debt, which granted is taxed at higher rates [in the US], but if chosen wisely (with good collateral) has returns that are much more predictable.”

Like other families keen on wealth preservation, Blennemann prefers strategies that can put his capital to work: “I don't rely on home runs and I don't mind if they are boring.”

Your personal foreign policy

Jonathan Lewis, co-founder and CIO of Samson Capital Advisors, believes every family probably has its own personal foreign policy and view of the world, even if they don't realise it.

“You might have doubts about Europe's recovery or be pessimistic about the Middle East – these types of opinions make up your own personal foreign policy. Families can become particularly troubled by their investments if they believe the portfolio isn't performing in line with their world view,” explains Lewis, who has authored two books on the intelligence community in the United States – Spy Capitalism: Itek and the CIA (Yale University Press, 2002) and Reflections of a Cold Warrior. “The challenge is to ensure that your view is reflected in your asset allocation model and that you can find the appropriate managers to execute it.”

“You might have doubts about Europe's recovery or be pessimistic about the Middle East – these types of opinions make up your own personal foreign policy. Families can become particularly troubled by their investments if they believe the portfolio isn't performing in line with their world view,” explains Lewis, who has authored two books on the intelligence community in the United States – Spy Capitalism: Itek and the CIA (Yale University Press, 2002) and Reflections of a Cold Warrior. “The challenge is to ensure that your view is reflected in your asset allocation model and that you can find the appropriate managers to execute it.”

Lewis says that gathering geopolitical and macroeconomic data or information is only the first step in the process: “The ease of access to data does not relieve the investor of their responsibility in decision-making.”

He recommends families try to articulate their view of the world and see how it can feed into their asset allocation: “What are your geopolitical views? Are you concerned about rising inequality, drought or hunger in certain regions? What are you interested in or care about? Do your investments reflect your opinions on geopolitics?”

However, even within the one geopolitical view there will be myriad permutations of how that view can be stated in the market. Lewis says families need to work carefully with their advisers and managers to ensure their beliefs are realised in a portfolio. At Samson's quarterly investment committee planning meetings, Lewis says committee members identify what they believe to be the key macro variables and formulate bull and bear scenarios.

While not necessarily recommending families follow such a structured approach to their planning, Lewis says it is important for families to be able to regularly articulate their world view and contemplate how it may play out in their asset allocation strategies.

With various geopolitical events threatening to impact the markets, how well prepared is your portfolio? Or do you believe fundamentals drive performance, devoid of influence from the “real” world?