Amundi on private markets: A strong value proposition that may emerge reinforced after the crisis

Covid-19 has created challenges for short-term investment performance and fundraising, but the longer-term prospects are strong and the capital shift to real assets will continue. In 2021, more than ever, real assets are likely to be a source of attractive risk adjusted returns.

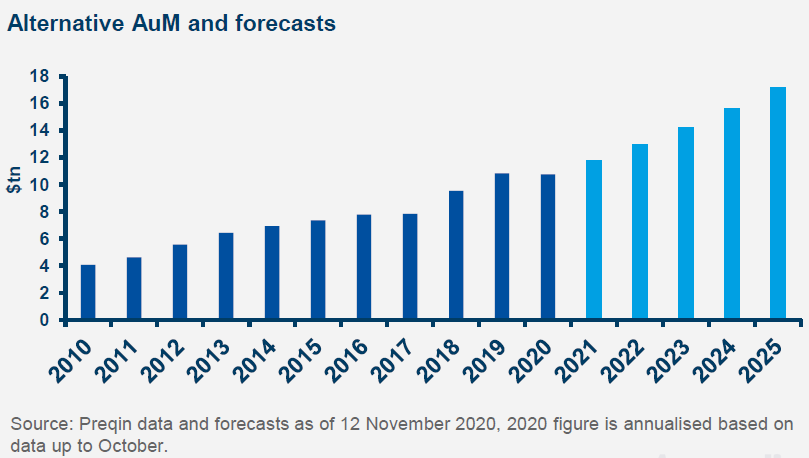

The Covid-19 crisis has caused significant disruption in private markets, with fundraising and deal making being impacted since the start of 2020. While activity is not at the record highs seen in recent years, funds are still raising capital and managers are putting money to work, as investor appetite for real assets stays unabated. Global private markets have topped $10 trillion in terms of assets under management, as of October 2020, and should grow up to $17.2 trillion by 2025 according to Preqin.

Most investors build their exposure to private markets via regular commitments, irrespective of market conditions. For investors looking for a good market timing, the Global Financial Crisis (GFC) showed that private capital funds that deployed money throughout the crisis produced among the strongest returns.

The GFC and the Covid-19 crisis are different in many ways. Currently, liquidity is abundant and CBs have been much more accommodative than they were in 2008-11. Fundraising will be supported by this liquidity. Market activity will benefit from the high level of dry powder.

Given the current market circumstances of low or negative interest rates and volatile equity markets, real assets offer among the best risk adjusted returns in the universe of investable assets. To capture the different premiums embedded in real asset investing, increased selectivity is mandatory. Only the best quality assets should be considered: Core and Core plus assets in RE and Infrastructure, senior secured instruments in PD, growth capital and LBO investing in the winning industries for PE. Private markets are witnessing strong divergences among sectors, and a dichotomy between healthy sectors with stable price and deal volumes, whereas some sectors are strongly affected by the crisis with almost no deal activity. Distinguishing the former from the latter is key to protect the income generation engine that real assets offer. Diversification in exposure and asset selection is key to benefit from what private markets can offer to long term investors.

Given the current market circumstances of low or negative interest rates and volatile equity markets, real assets offer among the best risk adjusted returns in the universe of investable assets. To capture the different premiums embedded in real asset investing, increased selectivity is mandatory. Only the best quality assets should be considered: Core and Core plus assets in RE and Infrastructure, senior secured instruments in PD, growth capital and LBO investing in the winning industries for PE. Private markets are witnessing strong divergences among sectors, and a dichotomy between healthy sectors with stable price and deal volumes, whereas some sectors are strongly affected by the crisis with almost no deal activity. Distinguishing the former from the latter is key to protect the income generation engine that real assets offer. Diversification in exposure and asset selection is key to benefit from what private markets can offer to long term investors.

Real assets are key in the strategic asset allocation as they are a portfolio diversifier and volatility dampener. Given their long-term nature, investors should not rush tactically into these assets and be selective in order to capture the different premiums embedded in real asset investing.

Private equity (PE)

Private equity (PE)

The PE market is sending messages that are complicated to interpret, as valuations have fallen relatively little, with a situation that is similar to the listed equity market that has not really fallen significantly either. However, for both listed and unlisted equity markets, this goes along with strong divergences between sectors, and the crisis exacerbates the winners vs losers’ state of play.

We see companies that are doing well with good cash flows or even emerging strengthened by the crisis vs companies that are doing less well, but may offer good opportunities in terms of entry prices. Despite the disruption, 2020 has been another active year for the PE industry globally and in Europe. European PE raised about €50 billion ($60.7 billion) in H120 in line with the first half of 2019.

In addition, investment remained resilient, with almost €40 billion ($48.6 billion) deployed and more than 3,000 companies backed and over 50 of the money directed at the IT, healthcare and biotech sectors, showing the key role that PE plays in innovation (European venture capital enjoyed a record half year, with investment approaching €13 billion/$15.8 billion).

PD should see a shift towards safer, more senior, and more secured strategies

Despite the adverse environment, European private debt funds have seen a rush of capital, raising €21 billion ($25.5 billion) in the first half of 2020 as investors seek to take advantage of potential counter cyclical investments. In the coming months, we will have to deal with the many difficult situations and restructuring processes.

In the coming months, we expect to see an acceleration in corporate consolidations in most sectors as many unlisted companies will emerge weakened from the crisis, with higher debt levels. Companies will need to strengthen their equity in some cases, significantly and many will not be able to find refinancing solutions through bank credit lines. Many small to medium businesses will have to call on private funding and PE. Structured equity can help entrepreneurs get through the crisis, and this is what PE funds using minority stakes investment strategies would typically do, mainly by using preference shares.

Overall, performances of PE funds should emerge stronger in the aftermath of the Covid-19 crisis, and we believe it is an extremely attractive time to invest in PE for investors who can bear some liquidity constraints. As evidenced by fundraising numbers, money has been funnelling into the asset class from long term investors, such as pension funds or insurance companies, and we expect the trend to continue in 2021 with the continuation of the crisis.

Private debt (PD)

Private debt (PD)

There are now a record high 486 funds on the road, seeking $239 billion in aggregate capital globally. This is quite aligned with LPs’ intentions that point to further growth over the medium-term for the asset class, with a 2% median current allocation vs a 3-4% target. LPs have appetite for PD because it provides better diversification, reliable income streams, high risk adjusted returns, and low volatility. Investors also appreciate the embedded option that is offered by PD over traditional liquid credit in the uncertain environment of the Covid-19 crisis i.e. the stringent financial documentation, the ability to restructure pricing or terms the floating rates the ability to repossess hard assets if needs be, and the option to exit at par.

In 2021, we will enter a new phase of the Covid crisis environment for PD, where we will see a lot of work being done on the portfolios with much significant restructuring. In terms of deal-making activity, investment opportunities should flourish for PD funds in the next 1-18 months, where we should see less banking competition, coupled with huge financing needs from issuers. Banks balance sheet have been highly mobilised in the past months with a lot of provisioning and an increased cost of risk that has led banks to reprice their credit offer.

We should see a lower level of banks’ underwriting for mid to large cap deals. For issuers, we expect the Covid-19 crisis to create opportunities in M&A and consolidation. The crisis has also highlighted the need to adapt most business models which will require capital expenditure, e.g. the length and complexity of supply chains or digital underinvestment, which will require capital expenditure. Finally, balance sheets’ re-leveraging will require indebtedness rescheduling, where PD’s bullet profile could emerge as a critical tool. The PD market is much larger than it was at the time of the GFC, and there is a lot of dry powder. With such an abundant capital available in the asset class, stringent selectivity will be key to deliver on PD’s promises.

We should see a lower level of banks’ underwriting for mid to large cap deals. For issuers, we expect the Covid-19 crisis to create opportunities in M&A and consolidation. The crisis has also highlighted the need to adapt most business models which will require capital expenditure, e.g. the length and complexity of supply chains or digital underinvestment, which will require capital expenditure. Finally, balance sheets’ re-leveraging will require indebtedness rescheduling, where PD’s bullet profile could emerge as a critical tool. The PD market is much larger than it was at the time of the GFC, and there is a lot of dry powder. With such an abundant capital available in the asset class, stringent selectivity will be key to deliver on PD’s promises.

We expect a flight to quality, with people wanting to invest in safer strategies, more senior, more secured, and in asset-based financing. This crisis will be a test for some LPs and GPs. We expect to see an increase in European defaults that should be concentrated in certain sectors e.g. airline, oil gas, travel/ leisure and typology of companies (poor governance, SMEs). Broad diversification in geography and sector will be paramount, together with investing at the top of the capital structure, where risk adjusted returns are the most attractive.

Real estate: opportunities from recent repricing, with differences among sectors

RE investment has solid fundamentals that can help investors to seize opportunities arising from fast growing trends in offices, retail or logistics. We see the crisis as an opportunity to adjust RE market value scales, focusing on core assets and diversification.

Real estate (RE)

Real estate (RE)

In the unprecdented and evolving context of the Covid-19 crisis, global RE markets saw a YoY decline in deal activity as of September 2020 and fund raising experienced a sharp YoY drop in 3Q20. While some investors opted for a wait and see attitude, the ongoing repricing in some market segments could attract new commitments. We believe the flight to quality observed since March should continue, on the back of the current uncertainty around the second wave of the pandemic. This should benefit core assets and properties whose tenants boast strong balance sheets Investors still feel comfortable transacting high quality assets, as the assets’ value should be more resilient than for secondary assets.

So far, repricing has hit risky assets, and we expect to see a scale of value among properties according to location, tenant’s financial robustness, and asset’s intrinsic features, something that had been dissipating before the crisis. This is especially true for properties on the periphery and those not dedicated to a specific business sector. We believe investors will monitor the leasing markets, particularly rents. The crisis has occurred in a healthy leasing market for logistics and offices in Europe, with an office vacancy rate that is on average lower than before the GFC. Despite a rise in 3Q20 office vacancy rates remain at low levels in the central business districts of the main European markets, limiting the impact on rents.

Low interest rates should support the recovery starting from high risk premiums on European prime real estate yields, many above 300bps as of September 2020. Finally, the impact of the pandemic is not linear, with some real estate sectors hit harder than others.

Low interest rates should support the recovery starting from high risk premiums on European prime real estate yields, many above 300bps as of September 2020. Finally, the impact of the pandemic is not linear, with some real estate sectors hit harder than others.

We expect the office sector to refocus on core assets and remain relatively unscathed for the best quality assets There are many long term leases in the market and many firms have been able to adapt to social distancing and are operating with a mobile workforce using technology. Remote working could accelerate, but without disputing that working from the office drives corporate culture, brand and team building.

Logistics has benefited from high e-commerce activity, with a greater need for industrial warehousing and logistics properties, although a multichannel retailing strategy should become the norm. Since investors see online retailing as a long-term trend, logistics properties can be pricy.

The boom in online sales has hit non-food shops harder. With new lockdowns in Europe, some retailers may have more difficulties paying high rents this time round.

Lastly, the hotel industry could suffer the effects of the crisis for longer, assuming its model is not called into question. Although the Covid-19 crisis strongly affected retail and hospitality, they could present some investment opportunities in the longer run, when market fundamentals get rebalanced.

Infrastructure

Infrastructure

Few investors were exposed to infrastructure during the GFC. Today, the asset class is undergoing its first global crisis and investors prize its ability to resist market turbulence. As for most private markets, we see divergences between sectors in terms of deal activity and valuation. The high level of dry powder that existed before the crisis is smoothing deal activity in ‘safe haven’ sectors such as health, technology or renewables, where a stable number of transactions is happening. In the most affected sectors, such as transportation or midstream energy, there might be opportunities at discount prices, whereas we might see some pricier assets in health or technology.

Overall, valuations should stay flattish. Such stability confirms a core feature of infrastructure its long-term time horizon. Prices may be more attractive in some sectors today, but it will not make a big difference in terms of returns in the long run.

Buy and hold strategies are gaining more traction in this environment. Infrastructure is a multi-faceted asset class that encompasses a complex mapping of risks, such as regulatory risks, political risks, country level risks, and industrial risks. We believe diversification is key in this asset class in order to deliver the stable return pattern that investors expect. Finally, the Covid-19 crisis should lead to a supportive political and regulatory environment, as the pandemic has emphasised the need for communication and social infrastructures, but also for more renewable energy.

Infrastructure projects should be a key component of most governmental stimulus plans, and we expect to see a rise in greenfield projects. In that context, private capital should play a vital role, as the crisis has put a strain on national debt in most countries.

Visit the Amundi Research Centre to read its complete Outlook 2021 for all its investment platforms, including equities, fixed income, emerging markets, multi-assets and real assets.

Visit the Amundi Research Centre to read its complete Outlook 2021 for all its investment platforms, including equities, fixed income, emerging markets, multi-assets and real assets.Important Information

Unless otherwise stated, all information contained in this document is from Amundi Asset Management S A S and is as of 12 November, 2020. Diversification does not guarantee a profit or protect against a loss. The views expressed regarding market and economic trends are those of the authors and not necessarily Amundi Asset Management S A S and are subject to change at any time based on market and other conditions, and there can be no assurance that countries, markets or sectors will perform as expected. These views should not be relied upon as investment advice, a security recommendation, or as an indication of trading for any Amundi product.

This material does not constitute an offer or solicitation to buy or sell any security, fund units or services Investment involves risks, including market, political, liquidity and currency risks. Past performance is not a guarantee or indicative of future results. Date of first use 18 November, 2020.