In search of the bottom in the Covid-19 crisis

In this unprecedented time of high uncertainty from a sanitary and economic perspective, the different drivers at play are moving in different directions. These forces make the exercise of GDP forecasting quite tricky and not particularly helpful for the time being.

As of the writing of this article on 25 March, 2020, markets are leading the real economic cycle and therefore they will bottom before the end of the pandemic. However, they will calm down and be reassured on the path forward when they can anchor expectations on three points:

1. The cyclical pattern of the pandemic, or when there is some sign of an improvement on the speed of the contagion. This depends on the “time” variable (the extension of the crisis period) and on the mobilisation efforts (the containment measures put in force in the different states). Early containment with strong measures such the ones applied in China and most recently in the main Western countries could help limit the spread of the virus;

1. The cyclical pattern of the pandemic, or when there is some sign of an improvement on the speed of the contagion. This depends on the “time” variable (the extension of the crisis period) and on the mobilisation efforts (the containment measures put in force in the different states). Early containment with strong measures such the ones applied in China and most recently in the main Western countries could help limit the spread of the virus;

2. The ‘whatever is necessary’ tactics of fiscal and monetary authorities, and whether or not monetary policies and fiscal measures are considered credible and effective to ease financial conditions for the corporate sector or to provide adequate resources to the household sector to face a period of higher unemployment due to the shutdown of economic activity;

3. The short end of the credit curve, after recent dislocations, and core bonds yields, which have started to rise since the fiscal measures have been announced, discounting higher future debt.

We should acknowledge that we are in a situation similar to October 2008, when uncertainty was very high, volatility was extreme and liquidity was vanishing. The market bottomed in March of the following year. However, this time extraordinary measures have been put in place at an earlier stage of the crisis (2008 was a lesson) and the stimulus is significantly bigger. Markets will take time to digest all these measures, but will start pricing in that they are unlimited.

We should acknowledge that we are in a situation similar to October 2008, when uncertainty was very high, volatility was extreme and liquidity was vanishing. The market bottomed in March of the following year. However, this time extraordinary measures have been put in place at an earlier stage of the crisis (2008 was a lesson) and the stimulus is significantly bigger. Markets will take time to digest all these measures, but will start pricing in that they are unlimited.

However, the policy bazookas will not be effective unless there is a corresponding fall in the speed of contagion. The combination of the two will drive the timing of the recovery and, as long as the pandemic does not seem to be under control, volatility will persist.

In our view, what matters most to investors is the speed (second derivative) of the pandemic’s direction. The direction is still pointing towards a rise in the number of cases, with an increasing speed in recent weeks. When the containment measures start working the speed should decelerate. This happened in China first and we now see some signs it is happening in Italy as well, which is helping to provide some relief to the market.

However, normality will not come directly after the pandemic is contained as some sort of social distancing (resulting in a higher percentage of smart working, higher online consumption, more online entertainment and online education, higher social media usage, increased demand and salary for medical jobs, etc.) will remain in place as long as a vaccine has not been found. This, again, is the case in China, where activity is slowly resuming after the lockdown but still remains below normal levels.

Most countries are still some way away from their peak, with the UK and the US still in an acceleration phase, as well as many EU countries, while some EM countries are still at an early stage. If this global lockdown proves successful, the pandemic should accelerate towards its peak in the next month, after which the speed in the growth of new cases should start to diminish.

We are moving in this direction, but we are not there yet and in the short term we can only expect temporary relief from the extreme market dislocation rather than a full and stable recovery.

Covid-19 cumulative number of cases by country

Source: Amundi on Bloomberg data, as at 17 March, 2020

A new financial regime has started: investment implications

We now acknowledge that “coronavirus” is the name of the invisible hand that drives the mean reversion process, bringing returns back on track with the long-term fundamental trend.

Equity returns had deviated from this in the last phase of the bull market and recently even overshot to the downside trends in productivity, labour force and earnings growth. Beyond the short-term pain, this is good news for the long-term sustainability of returns. However, in credit the unlimited quantitative easing will in some cases (the IG space, for example) postpone the moment of truth, while in the HY space defaults will inevitably rise as the economy contracts.

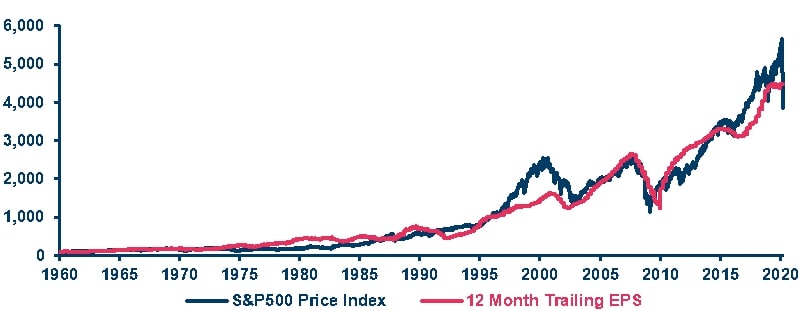

S&P500 Index vs Trailing EPS

Source: Amundi on Bloomberg data. Data as of 23 March 2020. S&P500 price index vs Trailing 12 Month EPS, rebased at 100 at 31 Dec 1959

Coronavirus is also the trigger of a regime shift. As we pointed out in our “Road back to the 70s” paper, the next recession (and this is what we have ahead in the coming months) will take monetary and fiscal policy to the next level. We will wake up the day after the pandemic ends with budgetary and monetary stances we would previously have considered unthinkable: the independence of central banks at the service of budgetary needs, helicopter money and unsustainable debt levels, with monetisation as a possible way out.

A re-appropriation from the States of some critical social functions that have been disregarded in recent years (healthcare, for example), the nationalisation of some companies or sectors (i.e., some airlines), the inshoring of activities and a shift towards wages from profits (see, as an example, the debate in the US about avoiding fiscal stimulus being used for corporate buybacks or to increase CEO pay) will all be new features of this new regime that will end up being inflationary in nature in the long term.

In this transitionary phase, as the crisis unfolds it will become clear to investors that the day after the pandemic ends they will find themselves with lower core bond yields and a need to find yield elsewhere. Credit and EM debt will be the natural candidates in the public markets, but at the moment the pressure on these asset classes remains high and it is not yet time to call aggressive entry points.

On credit, the downward migration of company ratings (from BBB IG to HY space) and defaults are the key challenges in a low liquidity environment. In the low-quality rating space, the focus is on companies that can survive a temporary lockdown of economic activity (lower/no earnings) with still regular and sometimes high costs (debt repayments): what was unsustainable before the crisis will be seriously challenged and result in defaults.

On credit, the downward migration of company ratings (from BBB IG to HY space) and defaults are the key challenges in a low liquidity environment. In the low-quality rating space, the focus is on companies that can survive a temporary lockdown of economic activity (lower/no earnings) with still regular and sometimes high costs (debt repayments): what was unsustainable before the crisis will be seriously challenged and result in defaults.

On EM, the current crisis is developing along with the oil crash. While monetary policy has decent room to move almost everywhere (thanks to falling inflationary pressures), not all countries will have the adequate fiscal room to manoeuvre to counteract the fall in commodity prices and the freeze in tourism activity; some countries will have to restructure their debt.

Active management and selection will be key to managing this “in-between phase” and in particular the trade-off between performance and liquidity. Now more than ever, robust liquidity management will make a difference. In credit we remain cautious and highly selective in the high yield space, while we prefer the IG space, which should benefit from the central banks’ umbrellas, as will peripheral bonds. The continuation of the downward loop in the market could only be justified by a permanent shock to potential growth, but this is not the most likely scenario right now. At current market price levels, about 10% default rates are expected (for US HY) and an earnings recession of 10-20% in the US market in 2020. This is certainly concerning, but not an Armageddon.

In terms of portfolio management, this backdrop calls for a still-cautious approach, as we recognise that global risk aversion will persist in the short term and will legitimately drive a flight to safety into a combination of high quality, defensive and liquid assets.

Equity markets will remain under pressure until signs of stabilisation in the curve of the epidemic’s evolution materialises. In equity, we see opportunities arising in quality cyclical sectors that could bounce back strongly once the appeal of cyclicals is restored as we approach the peak of the pandemic. Some bottoming out could begin earlier at a regional level. This is the case in China, which is now overperforming the rest of the world (the S&P 500 is down almost 27.6% from its peak—from 19 February to 24 March—while the Shenzhen CSI300 is down in USD terms only 11.3% in the same period) as it has likely passed the worst of the pandemic and its economy is already entering the bottoming-out phase.

The pickup in the dollar is temporary, in our view, and when the dust settles, it will be clear that looking at various risk premia in emerging markets and at the valuation of currencies, investors are being well paid for the risk of any further depreciation in the currencies.

In the illiquid world the real impact of the shock will surface as usual with a lag, coupled with the need to reprice, revisit valuations, review covenants and manage waivers. Ramp-ups and pipelines will come to temporary stops. This world is going through this review of the portfolios with the same focus on quality, price/valuation and the possible effective liquidation of assets.

A message on private assets from Pedro Arias (pictured), Global Head of Alternative & Real Assets at Amundi

A message on private assets from Pedro Arias (pictured), Global Head of Alternative & Real Assets at Amundi

1. Many institutional investors have increased their allocations to alternatives in a search for yield before the pandemic—will the search for yield intensify further in the years ahead?

Demand for private assets will remain strong. It is not their absolute performance that makes them attractive, it is their performance relative to listed comparable assets. This premium is linked to their low liquidity but also to the alpha that is inherent to these asset classes (“active ownership” creates value). Historically, this has been true throughout the crises.

2. Should investors increase or reduce their allocations to alternatives given that there were concerns about a bubble developing and private equity and worries about valuations in real estate and infrastructure.

Private market valuations will progressively adjust to the new environment. This will definitely provide very good investment opportunities. This said, we have always advised our clients invest stable amounts every year on these asset classes whatever the market conditions, in order to reduce their exposure to market cycles.

For the latest market insights, visit the Research Centre of Amundi Asset Management.