How to invest in Leveraged Loans in the current market environment

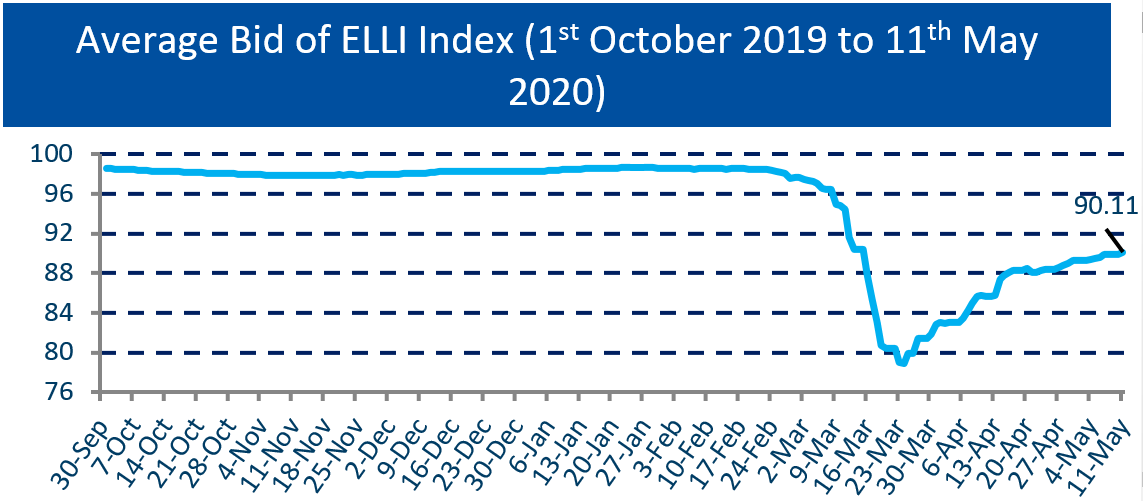

The European Leveraged Loans market—like other credit markets—suffered from a sudden and indiscriminate market price decrease at the beginning of the Covid-19 crisis in March, mainly resulting from lack of liquidity across all sub-investment markets and concerns about future rating downgrades and increased probability of defaults.

However, as a result of extensive government support across Europe, prices have staged an impressive recovery, which seems to us somewhat disconnected from the most challenging macro-economic environment that lies ahead.

A handful of companies have seized the opportunity of the relative strength of the market to issue new debt, mainly to extend the maturity of their existing financings. These issues—Loans and Floating Rate Notes—priced wider by 100 to 150 basis points than previous issues and have been well received.

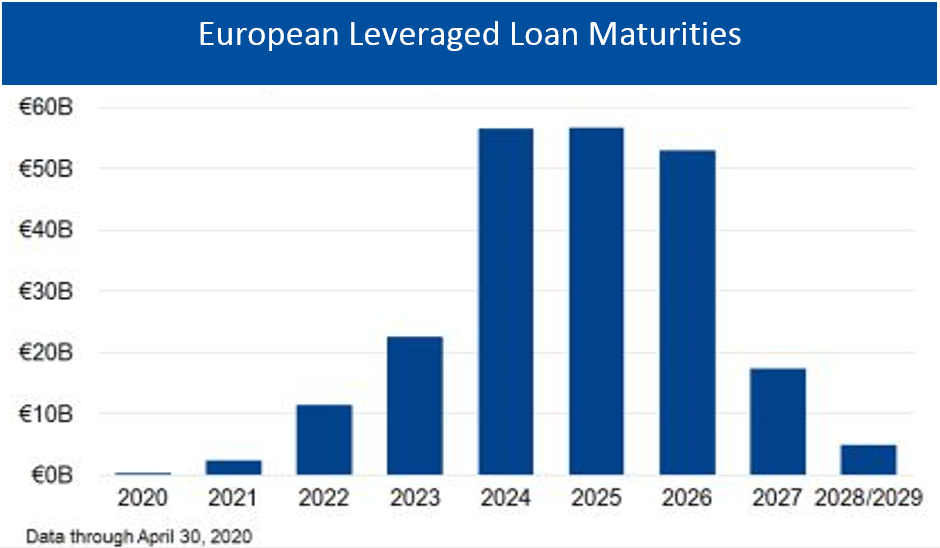

On the other hand, from a macro-perspective, as can be seen in the graph below, the European Leveraged Loan market does not have a short term maturity wall to address while the economy and the market are still in recovery phase.

In this context we maintain a selective and prudent approach to the management of our funds.

Amundi portfolio reactions

During March 2020, Amundi European Leveraged Loans funds have outperformed the market by 1 to 2%. We believe this can be attributed to the broadly diversified nature of the portfolios, a rigorous credit selection process and a focus on more defensive sectors.

While market prices of these loans are likely to fluctuate in the coming months, we have renewed our focus on monitoring each loan’s financial strength and flexibility (liquidity in particular), our position in the capital structure (Senior Secured Debt), the legal operating framework (law and country of the issuer) and our ability to trade the relevant loan. All these efforts are aimed at protecting the invested capital in the medium and long term.

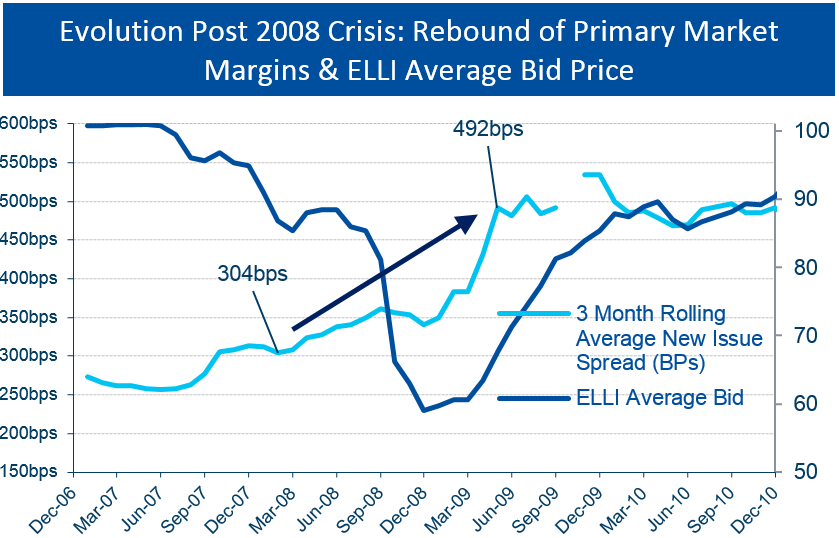

Takeaways from the previous crisis

1) Rise in margins

Based on the assumption that the evolution of the loan market post the GFC of 2008 provides a pertinent framework to inform us, we could anticipate how markets could react after the crisis and when the Leveraged Loans primary market reopens.

Similar to the 2008 to 2010 period, we may expect margins to increase: at this point we would anticipate margins to increase from 350bps to at least 450bps.

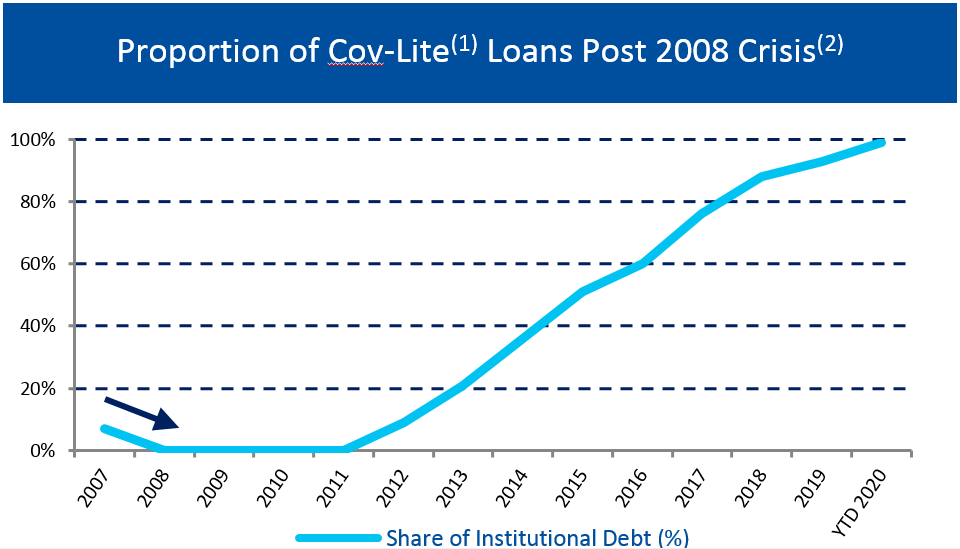

2) More protective documentation

Likewise, we may also see tighter loan documentation, possibly with a lower portion of “cov-lite” loans post the Covid-19 crisis. Cov-lite represented more than 90% of transactions in 2019.

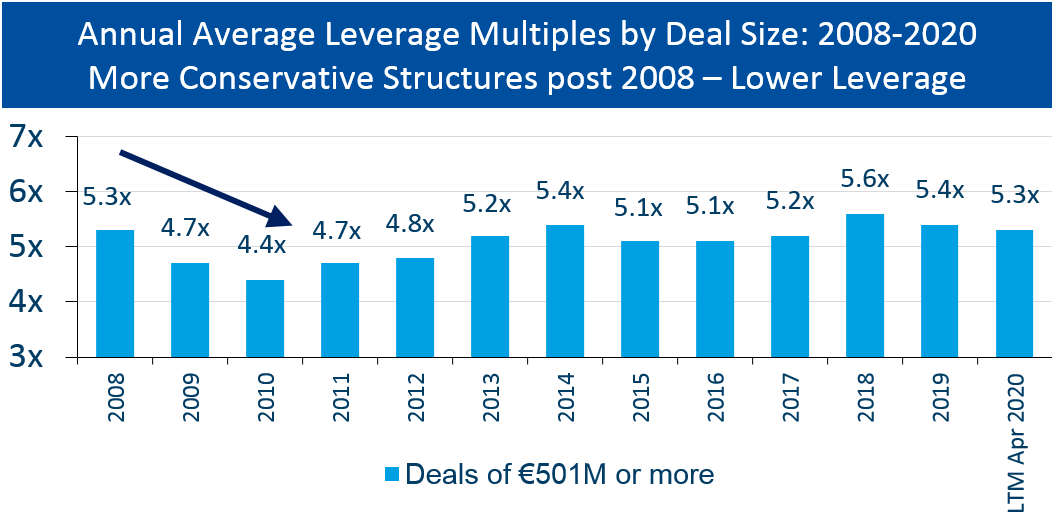

3) More conservative structures

We would also expect more conservative capital structures with lower leverage, as was reported post GFC when leverage reduced by almost one turn between 2008 and 2010.

Amundi view

While these changes would be positive to lenders we are still confident the Leveraged Loans market will remain an essential and attractive source of financing for Leveraged Buy-Out transactions due to the stability of the market and the inherent flexibility it brings to capital structures.

European-focused Private Equity asset managers have a record level of capital to invest c. €280 billion as of June 2019 (1). As in previous cycles, we believe Private Equity sponsors will be keen to participate in Mergers and Acquisitions resulting from Corporate restructurings post crisis.

European-focused Private Equity asset managers have a record level of capital to invest c. €280 billion as of June 2019 (1). As in previous cycles, we believe Private Equity sponsors will be keen to participate in Mergers and Acquisitions resulting from Corporate restructurings post crisis.

Reminder of Leveraged Loan key characteristics

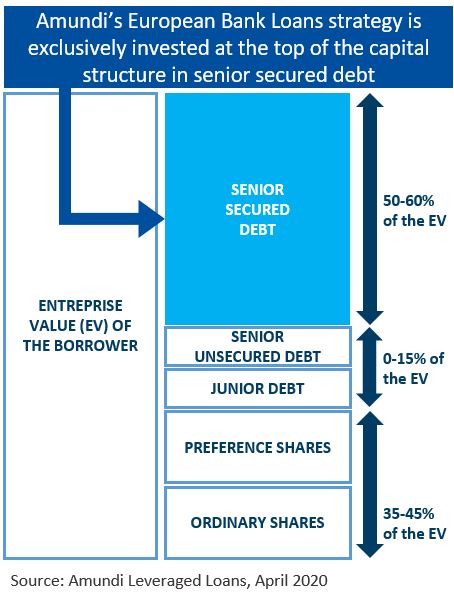

Leveraged Loans are senior secured debt positioned at the top of the capital structure providing good capital protection for investors.

As such, Leveraged Loans are secured on the borrower’s assets (buildings, intellectual property, patents, brands, shares of subsidiaries, bank accounts).

This “Senior Secured” status in the capital structure is also likely to provide better recovery as the debt has priority claims which are senior to other debt (unsecured debt, second lien, mezzanine) and equity. Over the period from 2000-2017 (including the GFC of 2008), Leveraged Loans exhibited a lower loss rate (aka cost of risk) than High Yield Bonds.

Amundi recently launched the second generation of its successful European bank loans fund. This successor fund is an open ended format, well-structured to allow prudent re-entry into the Leveraged Loans market, taking into account the challenging current macro-economic environment.

(1) Source: Preqin Pro, Preqin Global Private Equity & Venture Capital report, February 2020

Disclaimer: The information related to certain portfolio holdings (including portfolio holdings of funds) contained in this document (hereinafter the "Information") is provided to you by Amundi Asset Management S.A.S. (hereinafter “Amundi”) upon request and must be treated as strictly confidential.

Disclaimer: The information related to certain portfolio holdings (including portfolio holdings of funds) contained in this document (hereinafter the "Information") is provided to you by Amundi Asset Management S.A.S. (hereinafter “Amundi”) upon request and must be treated as strictly confidential.

This information is not of an advertising or promotional nature. It is not intended for and no reliance can be placed on this document by third parties, the public or retail clients, to whom the document should not be provided.

The Information is provided to you only on a personal, one-off basis at your request. By receiving this Information, you accept that you may not disclose it or allow it to be disclosed, in whole or in part, to third parties, in any way whatsoever and you undertake to take all the precautions and measures necessary for this purpose. You acknowledge that Amundi would suffer irreparable harm if you were to violate this confidentiality commitment and you agree that Amundi shall have recourse to all available legal remedies (including injunctive relief).

Nothing in this document constitutes investment advice, recommendation, solicitation, or offer to purchase or sell any securities or services described herein. Moreover, this information does not constitute an offer to sell or the solicitation of any offer to buy any securities or services in the United States or in any of its territories or possessions subject to its jurisdiction to or for the benefit of any U.S. Person (as defined in the prospectus of the fund/funds). The fund units/shares have not been registered in the United States under the Investment Company Act of 1940 and units/shares of the fund(s) are not registered in the United States under the Securities Act of 1933. It is the responsibility of investors to read the legal documents in force in particular the current prospectus for each fund.

The data contained in this document is as of the date of publication, except where otherwise stated and it shall only be used for internal compliance and evaluation purposes. It is important that you do not rely upon it to make investment decisions. Unless otherwise stated, all data contained herein is based on sources that Amundi considers to be reliable at the time of publication.

Data, opinions and analysis may be changed without notice. Amundi accepts no liability whatsoever, whether direct or indirect, that may arise from the use of information contained in this material. Amundi can in no way be held responsible for any decision or investment made on the basis of information contained in this material.